Have there been any updates to the payroll as of recently, ie PAYE modernisation, and if so what changes has it brought along as a result?

The most recent change came in 2019 with the introduction of the PAYE modernisation. It meant real-time reporting (RTR) as Revenue now follows the money. In other words, every time an employee receives a payment, Revenue must be informed on or before the day of payment. Otherwise, you may attract revenue attention and fines.

The modernisation saw the abolition of the “P” forms such as P45, P35, etc. The introduction of the revenue payroll notification (RPN) replaced the old tax certificate, while the payroll submission report replaced the P35. Before calculating payroll (regardless of frequency), an employer is obliged to request an RPN. If an out-of-date RPN is used, it is frowned upon by Revenue and you are at risk of a fine. We have observed that employee tax affairs are addressed promptly, and it is highly unusual to have new recruits on emergency tax.

Employers must notify Revenue via a payroll submission request of payments made to employees on or before payday. Any delays in getting these reports to Revenue are not welcome and can lead to fines and increase the risk of an audit.

Before a contractor takes on a new employee, what are the first steps they should take and what information do they require?

For payroll, a contractor needs to get the name, address and PPS number of an employee in advance of taking them on. They must then notify Revenue by requesting an RPN, normally via their payroll software. If one has agreed a take-home pay with an employee, the RPN will determine the cost of employment.

It is crucial that the RPNs are monitored as credits may go up or down depending on the individual’s circumstances. If an employer has agreed to pay gross (before tax), an RPN is requested from Revenue. The tax credit amount and standard rate cut-off point is less of a concern for the contractor as they do not influence the cost of employment.

Within five days of an employee starting, legally, the contractor is obliged to provide her/him a statement of the following five core terms of employment:

Full name of the employer and employee. Address or principal place of business of the employer in the State. Fixed-term/specified purpose contracts – expected duration/expiry date. Rate or method of calculation of employee’s remuneration and pay reference period for purpose of National Minimum Wage Act 2000. Number of hours which the employer reasonably expects the employee to work (a) per normal working day and (b) per normal working week.A written statement of terms and conditions governing their employment is to be issued no later than two months after their start date. Most employers issue a contract of employment that includes the five core terms and the statement of terms and conditions within the first five days of an employee starting with them.

Would you advise contractors to pay staff a gross wage rather than a net wage and why?

Contractors should never quote a net wage. It is almost impossible to quantify the cost to the employer at the outset. Although not as common as it used to be, we still come across employers negotiating a net rather than a gross wage when taking on a new employee. Even if you only have one person on your payroll, this can be an expensive mistake.

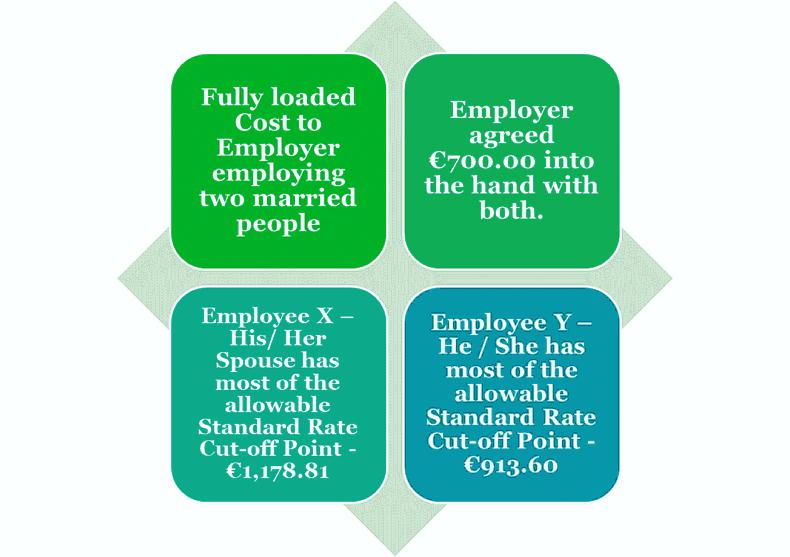

A net pay agreement is where you agree to pay a set amount ‘into the hand’. These arrangements are difficult to budget as they involve grossing up an employee’s pay to take into account tax, PRSI and USC and, in some cases local property tax liabilities. These liabilities can vary significantly from one employee to another as can be seen in Example A where there is a difference of €265.21 between two married employees on take home pay of €700 each.

In effect, by agreeing a ‘net’ wage, you are covering your employee’s deductions for them. Worse still, if income tax rates rise or your employee’s tax credits change, you will incur additional costs.

Net to Gross- Example A- Cost to the employer of employing two married people on same net pay of €700/week.

Failing to obtain PPS number

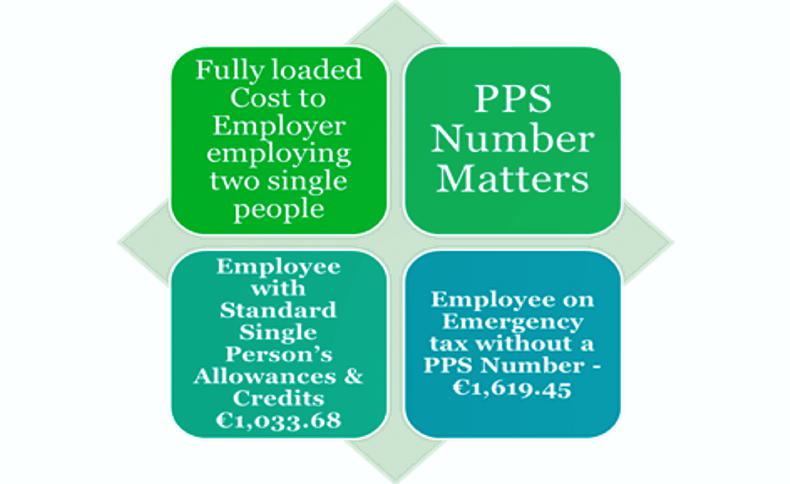

Failing to obtain an employee’s PPS number is another expensive mistake as the employee will be on emergency tax.

In Example B, agreeing ‘net’ pay with an employee on emergency tax costs €585.77 more than the employing the same individual when you know their PPS.

Net to Gross- Example B: Cost of employing a single person on €700/week net.

So, if you plan to take on new employees in 2022, remember that wage negotiations should always be based on gross wages. Where existing employee wages are based on take-home rather than gross pay, this is a good time to start phasing these arrangements out. For further information and/or advice contact ifac HR and payroll services.

Should contractors pay staff on a weekly, fortnightly or monthly basis and why?

The pay frequency is a matter for the contractor, it has no impact on overall employer costs. However, paying monthly would reduce administration and the payroll outsourcing costs.

If a contractor employs a driver part-time during the busy silage season, but that person is elsewhere fully employed, and thus their tax credits are used up, what is the cost of employment to the contractor?

In a nutshell, if one agrees a net pay the cost could be substantial and would depend on the individual’s pay situation. If a gross pay is agreed with an employee, it has no impact on the cost of employment.

If contractors have students working over the summer, and they prefer to get paid later in the year, this is OK. Remember, Revenue is only interested in the day you pay your employees, not when the Zwork was carried out.

If I, as a contractor, trade as sole trader or a limited company, does this have any impact on the process of paying my employees?

The business structure has no impact on the processing of payroll.

If an employer misses a payroll deadline, are they liable to be fined?

A breach such as a late submission can attract a €4,000 fine as does not having an up-to-date RPN for employees. Bear in mind it is €4,000.00 per breach.

Is there any tax-free incentive that contractors could avail of when paying staff?

Once a year, employers are allowed to give their employees a tax-free non-cash benefit of up to €500. This can only be a voucher, such as a One4All or supermarket voucher, and cannot be cash. Unlike cash bonuses which are taxable, benefits provided under the Small Benefit Exemption Scheme do not have to be put through payroll and are not liable for PAYE, PRSI or USC. This is a very cost-effective way of incentivising employees or thanking them.

"Remember, revenue is only interested in the day you pay your employees, not when the period of work was carried out".

\ Houston Green

Have there been any updates to the payroll as of recently, ie PAYE modernisation, and if so what changes has it brought along as a result?

The most recent change came in 2019 with the introduction of the PAYE modernisation. It meant real-time reporting (RTR) as Revenue now follows the money. In other words, every time an employee receives a payment, Revenue must be informed on or before the day of payment. Otherwise, you may attract revenue attention and fines.

The modernisation saw the abolition of the “P” forms such as P45, P35, etc. The introduction of the revenue payroll notification (RPN) replaced the old tax certificate, while the payroll submission report replaced the P35. Before calculating payroll (regardless of frequency), an employer is obliged to request an RPN. If an out-of-date RPN is used, it is frowned upon by Revenue and you are at risk of a fine. We have observed that employee tax affairs are addressed promptly, and it is highly unusual to have new recruits on emergency tax.

Employers must notify Revenue via a payroll submission request of payments made to employees on or before payday. Any delays in getting these reports to Revenue are not welcome and can lead to fines and increase the risk of an audit.

Before a contractor takes on a new employee, what are the first steps they should take and what information do they require?

For payroll, a contractor needs to get the name, address and PPS number of an employee in advance of taking them on. They must then notify Revenue by requesting an RPN, normally via their payroll software. If one has agreed a take-home pay with an employee, the RPN will determine the cost of employment.

It is crucial that the RPNs are monitored as credits may go up or down depending on the individual’s circumstances. If an employer has agreed to pay gross (before tax), an RPN is requested from Revenue. The tax credit amount and standard rate cut-off point is less of a concern for the contractor as they do not influence the cost of employment.

Within five days of an employee starting, legally, the contractor is obliged to provide her/him a statement of the following five core terms of employment:

Full name of the employer and employee. Address or principal place of business of the employer in the State. Fixed-term/specified purpose contracts – expected duration/expiry date. Rate or method of calculation of employee’s remuneration and pay reference period for purpose of National Minimum Wage Act 2000. Number of hours which the employer reasonably expects the employee to work (a) per normal working day and (b) per normal working week.A written statement of terms and conditions governing their employment is to be issued no later than two months after their start date. Most employers issue a contract of employment that includes the five core terms and the statement of terms and conditions within the first five days of an employee starting with them.

Would you advise contractors to pay staff a gross wage rather than a net wage and why?

Contractors should never quote a net wage. It is almost impossible to quantify the cost to the employer at the outset. Although not as common as it used to be, we still come across employers negotiating a net rather than a gross wage when taking on a new employee. Even if you only have one person on your payroll, this can be an expensive mistake.

A net pay agreement is where you agree to pay a set amount ‘into the hand’. These arrangements are difficult to budget as they involve grossing up an employee’s pay to take into account tax, PRSI and USC and, in some cases local property tax liabilities. These liabilities can vary significantly from one employee to another as can be seen in Example A where there is a difference of €265.21 between two married employees on take home pay of €700 each.

In effect, by agreeing a ‘net’ wage, you are covering your employee’s deductions for them. Worse still, if income tax rates rise or your employee’s tax credits change, you will incur additional costs.

Net to Gross- Example A- Cost to the employer of employing two married people on same net pay of €700/week.

Failing to obtain PPS number

Failing to obtain an employee’s PPS number is another expensive mistake as the employee will be on emergency tax.

In Example B, agreeing ‘net’ pay with an employee on emergency tax costs €585.77 more than the employing the same individual when you know their PPS.

Net to Gross- Example B: Cost of employing a single person on €700/week net.

So, if you plan to take on new employees in 2022, remember that wage negotiations should always be based on gross wages. Where existing employee wages are based on take-home rather than gross pay, this is a good time to start phasing these arrangements out. For further information and/or advice contact ifac HR and payroll services.

Should contractors pay staff on a weekly, fortnightly or monthly basis and why?

The pay frequency is a matter for the contractor, it has no impact on overall employer costs. However, paying monthly would reduce administration and the payroll outsourcing costs.

If a contractor employs a driver part-time during the busy silage season, but that person is elsewhere fully employed, and thus their tax credits are used up, what is the cost of employment to the contractor?

In a nutshell, if one agrees a net pay the cost could be substantial and would depend on the individual’s pay situation. If a gross pay is agreed with an employee, it has no impact on the cost of employment.

If contractors have students working over the summer, and they prefer to get paid later in the year, this is OK. Remember, Revenue is only interested in the day you pay your employees, not when the Zwork was carried out.

If I, as a contractor, trade as sole trader or a limited company, does this have any impact on the process of paying my employees?

The business structure has no impact on the processing of payroll.

If an employer misses a payroll deadline, are they liable to be fined?

A breach such as a late submission can attract a €4,000 fine as does not having an up-to-date RPN for employees. Bear in mind it is €4,000.00 per breach.

Is there any tax-free incentive that contractors could avail of when paying staff?

Once a year, employers are allowed to give their employees a tax-free non-cash benefit of up to €500. This can only be a voucher, such as a One4All or supermarket voucher, and cannot be cash. Unlike cash bonuses which are taxable, benefits provided under the Small Benefit Exemption Scheme do not have to be put through payroll and are not liable for PAYE, PRSI or USC. This is a very cost-effective way of incentivising employees or thanking them.

"Remember, revenue is only interested in the day you pay your employees, not when the period of work was carried out".

\ Houston Green

This is a subscriber-only article

This is a subscriber-only article

SHARING OPTIONS: