Firstly, farmer shareholders will question why they should sell 3% of their investment in a high-growth, high-margin and highly profitable business to buy 60% of a consumer foods and agribusiness that is seen to be mature, has stagnant growth and lagging margins.

After all, Glanbia’s star performance nutrition business makes margins in excess of 16% and its ingredients business makes margins in excess of 9%. Meanwhile, the consumer foods and agribusiness makes margins less than 5%.

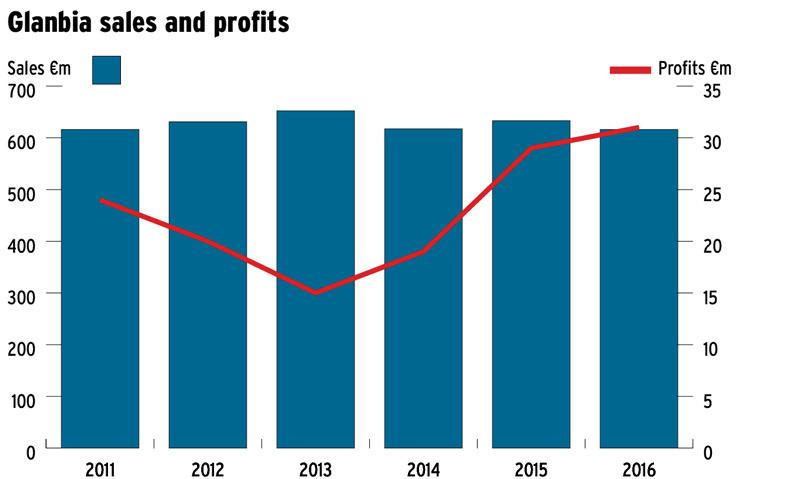

But as any investor knows, margin is only part of the story. A far better performance metric is return on invested capital. And although margins are weaker, this is a cash generative business. It must not be overlooked that it is a profitable business generating €25m to €30m every year.

Therefore, the question becomes one of value and are farmers overpaying for this business. Shareholders are being asked to spend €112m, or seven to eight times profits, to buy 60% of a profitable and stable business that fits the co-op and GII well. While there are complexities around pensions and working capital, it would seem like a reasonable number for this type of business.

Capital

A key part of this deal is that it cleans up the plc and frees up capital so that the plc can invest in higher-return businesses. Glanbia will now be seen and valued as a pure ingredients and performance nutrition business.

Institutional investors like clear business models, prefer lower levels of farmer ownership and pay higher values (price earnings) for ingredients businesses.

As the largest investors in the plc, the question then becomes should farmers welcome this higher valuation? Obviously, the higher the plc is valued, the greater the value of the co-op.

For example, since the announcement last week, shares in Glanbia have soared by 8% or €1/share. With the co-op holding about 100m shares, it means the co-op’s value has increased by €100m in the past week, almost the same value of the 60% they are going to buy.

The next question then becomes if this such a good deal, is valued fairly and is positive for the plc, why do farmers need a share spin-out sweetener to get this deal across the line?

Following the last spin-out two years ago, technically the co-op has the leeway to sell a further 3% of its plc shares to buy this business without going to shareholders. But the co-op is also proposing that an additional 2% be spun out, so a vote is needed.

For the dairy farmer, the deal to buy 60% of a consumer foods business makes pretty good sense. The dairy farmer has seen the value of having a well-invested processing arm, which did not require him/her to put his hand in his pocket to build. He/she has also seen the value of the milk supports during 2015 and 2016, when about €35m per year was paid out, the equivalent of almost 2c/l.

However, the dry shareholder, typically livestock or tillage, may feel a little short-changed. After all, what use is a cheese plant or powder plant to him/her?

While they do get an annual co-op dividend of about 10c per share, they also receive top-ups on grain (€10/t), and rebates on feed and fertiliser (€7/t). The plc share spin-out, which will yield €2,500 for every 1,000 co-op shares held even by a dry shareholder, will no doubt help sway their vote.

Then the last piece of this very complex jigsaw will be why the need to create a €40m member support fund? After all, this is farmers’ money that the co-op will use over time to support prices when markets are weak.

Clearly this brings a non-market dimension into the pricing of grain, feed, milk and fertiliser. It was particularly seen last year when Glanbia plc paid the market price for grain before the co-op boosted the price by €10/t. This distorted the market, forcing other merchants and co-ops to pay over the odds for grain. While this is positive for the farmer (in the short term), it may not be in the long-term interest of the wider industry.

The next question is how will the money flow back to farmers. Farmers must trade with the co-op to gain their share of the dividend coming from their investment in the co-op and hence plc. However, it becomes even more complex. If two farmers are equal co-op shareholders, but one has double the cows and milk of the other, then the larger farmer receives a larger dividend through member supports. Farmers may question if this is equitable and in the co-op way.

Minimum stake

Then with all this spinning out, there is the final question of what is the minimum stake the co-op should continue to hold in the plc?

Shareholders might ask what is the benefit of owning a 30% investment in a plc, when the only direct tangible benefit is that it will return a dividend of about €11m to the co-op each year.

However, since this news broke last week, it has been rumoured that a multinational could make a takeover bid for Glanbia’s sports nutrition and ingredients business.

While very much speculation, it is something that could become reality in the future, which farmers may need to consider. The co-op’s 36% stake in the plc is worth about €2bn. If this did happen the co-op would have the first choice to buy out the 40% plc share of Glanbia Ireland.

In doing this, they would have plenty of change from €1bn, leaving a very full cheque book to allow further acquisitions in excess of €1bn.

If the co-op took back full control of Glanbia Ireland, which is estimated to make €48m, this loss of the plc dividend could be made up by the gain of the plc share of the €48m profits. As Glanbia plc is still growing at double-digit rates, the co-ops investment is increasing too.

Alternatively, instead of buying a business, if it ever sold its shares, the co-op could write a cheque for €130,000 to each of its 15,000 shareholders. While the dry shareholders may welcome this outcome, as any farmer knows, you can only sell a field once.

Read more

Glanbia co-op shareholders in line for €10,000 spin-out boost

What’s behind the Glanbia deal?

Editorial: Glanbia proposal – questions to be asked

Firstly, farmer shareholders will question why they should sell 3% of their investment in a high-growth, high-margin and highly profitable business to buy 60% of a consumer foods and agribusiness that is seen to be mature, has stagnant growth and lagging margins.

After all, Glanbia’s star performance nutrition business makes margins in excess of 16% and its ingredients business makes margins in excess of 9%. Meanwhile, the consumer foods and agribusiness makes margins less than 5%.

But as any investor knows, margin is only part of the story. A far better performance metric is return on invested capital. And although margins are weaker, this is a cash generative business. It must not be overlooked that it is a profitable business generating €25m to €30m every year.

Therefore, the question becomes one of value and are farmers overpaying for this business. Shareholders are being asked to spend €112m, or seven to eight times profits, to buy 60% of a profitable and stable business that fits the co-op and GII well. While there are complexities around pensions and working capital, it would seem like a reasonable number for this type of business.

Capital

A key part of this deal is that it cleans up the plc and frees up capital so that the plc can invest in higher-return businesses. Glanbia will now be seen and valued as a pure ingredients and performance nutrition business.

Institutional investors like clear business models, prefer lower levels of farmer ownership and pay higher values (price earnings) for ingredients businesses.

As the largest investors in the plc, the question then becomes should farmers welcome this higher valuation? Obviously, the higher the plc is valued, the greater the value of the co-op.

For example, since the announcement last week, shares in Glanbia have soared by 8% or €1/share. With the co-op holding about 100m shares, it means the co-op’s value has increased by €100m in the past week, almost the same value of the 60% they are going to buy.

The next question then becomes if this such a good deal, is valued fairly and is positive for the plc, why do farmers need a share spin-out sweetener to get this deal across the line?

Following the last spin-out two years ago, technically the co-op has the leeway to sell a further 3% of its plc shares to buy this business without going to shareholders. But the co-op is also proposing that an additional 2% be spun out, so a vote is needed.

For the dairy farmer, the deal to buy 60% of a consumer foods business makes pretty good sense. The dairy farmer has seen the value of having a well-invested processing arm, which did not require him/her to put his hand in his pocket to build. He/she has also seen the value of the milk supports during 2015 and 2016, when about €35m per year was paid out, the equivalent of almost 2c/l.

However, the dry shareholder, typically livestock or tillage, may feel a little short-changed. After all, what use is a cheese plant or powder plant to him/her?

While they do get an annual co-op dividend of about 10c per share, they also receive top-ups on grain (€10/t), and rebates on feed and fertiliser (€7/t). The plc share spin-out, which will yield €2,500 for every 1,000 co-op shares held even by a dry shareholder, will no doubt help sway their vote.

Then the last piece of this very complex jigsaw will be why the need to create a €40m member support fund? After all, this is farmers’ money that the co-op will use over time to support prices when markets are weak.

Clearly this brings a non-market dimension into the pricing of grain, feed, milk and fertiliser. It was particularly seen last year when Glanbia plc paid the market price for grain before the co-op boosted the price by €10/t. This distorted the market, forcing other merchants and co-ops to pay over the odds for grain. While this is positive for the farmer (in the short term), it may not be in the long-term interest of the wider industry.

The next question is how will the money flow back to farmers. Farmers must trade with the co-op to gain their share of the dividend coming from their investment in the co-op and hence plc. However, it becomes even more complex. If two farmers are equal co-op shareholders, but one has double the cows and milk of the other, then the larger farmer receives a larger dividend through member supports. Farmers may question if this is equitable and in the co-op way.

Minimum stake

Then with all this spinning out, there is the final question of what is the minimum stake the co-op should continue to hold in the plc?

Shareholders might ask what is the benefit of owning a 30% investment in a plc, when the only direct tangible benefit is that it will return a dividend of about €11m to the co-op each year.

However, since this news broke last week, it has been rumoured that a multinational could make a takeover bid for Glanbia’s sports nutrition and ingredients business.

While very much speculation, it is something that could become reality in the future, which farmers may need to consider. The co-op’s 36% stake in the plc is worth about €2bn. If this did happen the co-op would have the first choice to buy out the 40% plc share of Glanbia Ireland.

In doing this, they would have plenty of change from €1bn, leaving a very full cheque book to allow further acquisitions in excess of €1bn.

If the co-op took back full control of Glanbia Ireland, which is estimated to make €48m, this loss of the plc dividend could be made up by the gain of the plc share of the €48m profits. As Glanbia plc is still growing at double-digit rates, the co-ops investment is increasing too.

Alternatively, instead of buying a business, if it ever sold its shares, the co-op could write a cheque for €130,000 to each of its 15,000 shareholders. While the dry shareholders may welcome this outcome, as any farmer knows, you can only sell a field once.

Read more

Glanbia co-op shareholders in line for €10,000 spin-out boost

What’s behind the Glanbia deal?

Editorial: Glanbia proposal – questions to be asked

This is a subscriber-only article

This is a subscriber-only article

SHARING OPTIONS: