This is a subscriber-only article

This is a subscriber-only article

Milk price cuts hit home hard in February as processors reacted to cuts in dairy commodity prices last autumn. The depth of the cut in prices, by up to 3c/litre, surprised and infuriated farmers in equal measure.

The impact of weather woes did nothing to soften the blow.

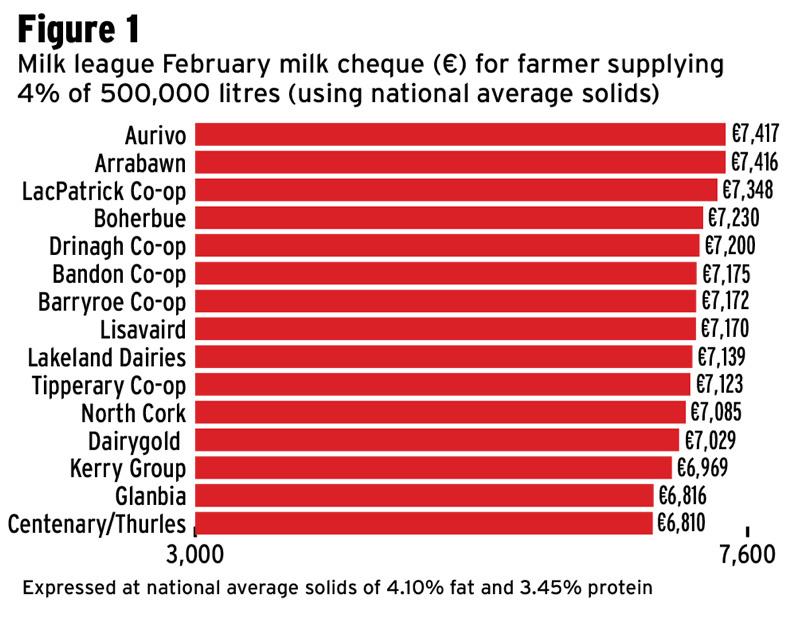

The inclusion of unconditional payments (paid to all suppliers) in the February milk cheque pushes Arrabawn, Aurivo and LacPatrick to the top of the February monthly milk league.

All three have an “early calving” payment or an added bonus on all litres supplied in February to try to incentivise farmers to supply more February milk.

Arrabawn comes out on top because while it dropped base price, it has started a 2c/l calving payment to match neighbouring processors. Aurivo and LacPatrick have had this for the last number of years.

After that, the west Cork co-ops hold the middle ground and indeed you would expect will regain the front when the early calving payments stop in March.

The big-volume players have set up home in division three. Dairygold, Kerry Group and Glanbia are in the bottom four, with the Glanbia base price of 10c per kilo milk solids (0.7c/l) behind Kerry.

Average February price

The average Irish price ex-VAT for the February monthly milk league is €4.61/kg MS at national average milk solids. The average price at 3.3% protein and 3.6% fat is 32.85c/l ex-VAT. All prices are quoted ex-VAT and exclude SDAS bonuses and conditional bonuses such as cell count bonuses, etc.

February milk cheque

Despite the fact that typically only 4% of annual supply is delivered in February, when we compare the processors’ milk prices at the same milk solids (national average) there is €607 of a difference in the base February milk cheque.

Figure 1 shows the difference in payout between processors for the standardised litre at 3.45% protein and 4.10% fat supplied during the month of February. It shows the difference in the February milk cheque for a supplier with a normal seasonal spring supply curve (4% in February) for a farm that will produce 500,000 litres in the year.

Actual price paid

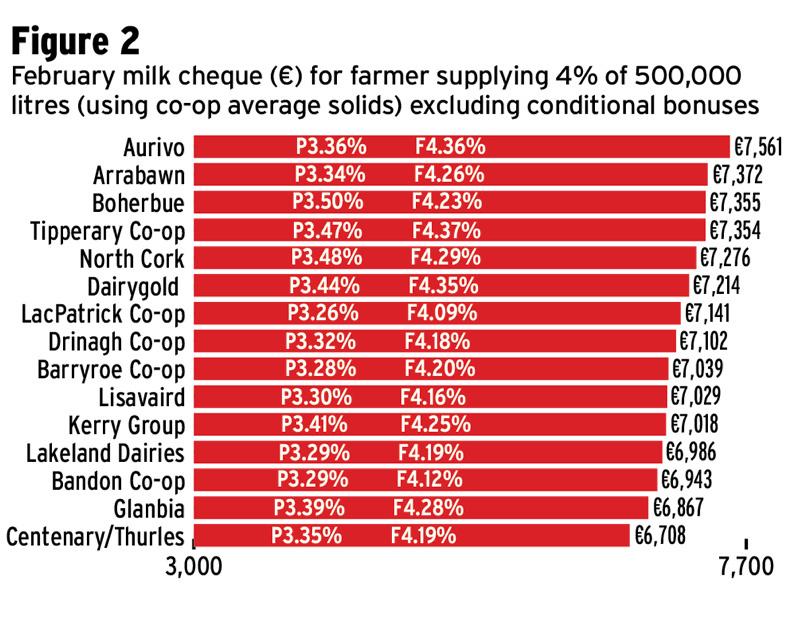

Figure 2 shows the difference in the actual February milk cheque delivered. When I say “actual”, I mean the money paid out for the different milk solids collected.

Milk processors collect milk that varies in fat and protein percentage so in effect the quality of milk goes some way to deciding the milk price paid out. The processor can’t pay top price if the quality is poor. The higher the milk solids (fat and protein) the higher the milk cheque.

National milk supply

Some processors in the south and east are experiencing milk supply reductions and low protein percentages. Glanbia, the largest processor in the east, is down 5% on March milk supplies and processors in the south and east report more milk coming in at 3%, which is well below seasonal norms.

Based on the low growth rates, average grass covers on most farms are expected to remain tight for the next two to three weeks. Farmers should discuss options with their co-op and advisers as there are solutions available. Careful management will be required over the coming weeks to avoid running out of both grass and silage.

LacPatrick payment changes

To further incentivise the delivery of milk with higher milk solids, LacPatrick has improved how it pays for milk from 1 April 2018. Instead of a quality bonus on top of the milk solids payment, the milk solids payment will now carry the full value as per most other processors. Milk quality penalties will apply instead. Instead of a 0.5c/l penalty for milk over 30,000 TBC, this has been raised to 1c/l. The base price for SCC is 250,000 cells/ml. The volume deduction (the C part of the A+B-C) is being increased from 3.5c/l to 4.5c/l, with this 1c/l difference transferred to the milk solids payment. Essentially, LacPatrick is rewarding higher protein and butterfat even more than it was. At baseline solids, the co-op says it’s worth an extra 3c/l.

New Zealand

Fonterra increased milk price last week for 2018. The New Zealand dairy giant increased its forecast milk price for the 2017/2018 season to $6.55/kg of milk solids (26.4c/l). In a statement, the farmer-owned co-op said the global demand for dairy remains strong, which was supporting product prices.

Remember, most New Zealand dairy farmers have the majority of their milk supplied for the 2017-2018 season. Fonterra said its dairy farmer suppliers can expect to receive a year-ending milk price payout of $6.80/kg MS to $6.90/kg MS (27.4c/l to 27.8c/l), which would be the third-highest payout for Fonterra suppliers over the last decade.

Drought affected the Fonterra supply and it recorded an 11% decline in volume collections to 10.5bn litres after the severe drought in November and December. This resulted in the co-op having 6% less product for sale than the same period last year.

A2 milk

Interestingly, I see Fonterra is entering a joint venture with the A2 milk company after years of talking down the product. New Zealand has many large-scale farmers who have been DNA-testing cows for the last number of years and can re-organise their herds very quickly to supply pure A2 milk. Rightly or wrongly, Fonterra has decided it needs an A2 brand to sell dairy products that are free of A1 beta casein.

GDT milk price

Prices at the most recent Global Dairy Trade (GDT) fell as well as milk prices for February supplies. Skim milk powder prices fell 9% at the GDT auction, dragging the overall GDT index down 1.2%.

Europe

Recent cold weather and tight feed supplies allied with poor feed availability are likely to put the brakes on EU milk supply. Butter prices and future butter markets look firm at €4,800/t. Cheese markets are also steady with cheddar prices flat at €3,200/t. Last week, only a bucketful of skim powder was sold out of intervention at €1,050/t.

SHARING OPTIONS: