Analysis of June milk prices suggests that some Republic of Ireland-based co-ops are currently paying up to 1.2p/l less for milk in NI than is being paid to their suppliers south of the Irish border.

With the euro continuing to trade strongly against sterling, the expectation among farmers is that co-ops should move to close the gap for July supplies. Sources in the trade acknowledge that the market can support higher prices, but caution that a base of 28.5p is towards the top end of what is possible at present.

Currently over half of the milk produced in NI is bought by co-ops based in the Republic of Ireland. The latest base milk prices announced for June across the main buyers of Lakeland, LacPatrick, Glanbia Milk and Aurivo in the Republic of Ireland were (excluding VAT) 31.3c/l, 31.54c/l, 31.22c/l and 31.78c/l, respectively.

This is for milk of 3.6% butterfat and 3.3% protein.

In NI, the payment system is different, with the base generally set at 3.8% to 3.85% butterfat and 3.15% to 3.19% protein. However, taking each base price, and applying quality adjustments (for NI suppliers), the higher protein percentage in the Republic of Ireland is mostly cancelled out by the higher fat percentage in the North. In general, the adjustments are slightly to the favour of southern suppliers, so it would be reasonable to expect the NI base price to be up to 0.2p/l ahead of a Republic of Ireland price.

It all means that the main factor driving differences in base prices either side of the border is the euro to sterling exchange rate. Taking the prevailing rate last week of €1=0.88p, the June 2017 base milk prices south of the border equate to 27.5p, 27.7p, 27.5p and 28p for Lakeland, LacPatrick, Glanbia Milk and Aurivo, respectively. These prices are between 0.5p/l and 1.2p/l more than what is actually on offer as a base to NI suppliers.

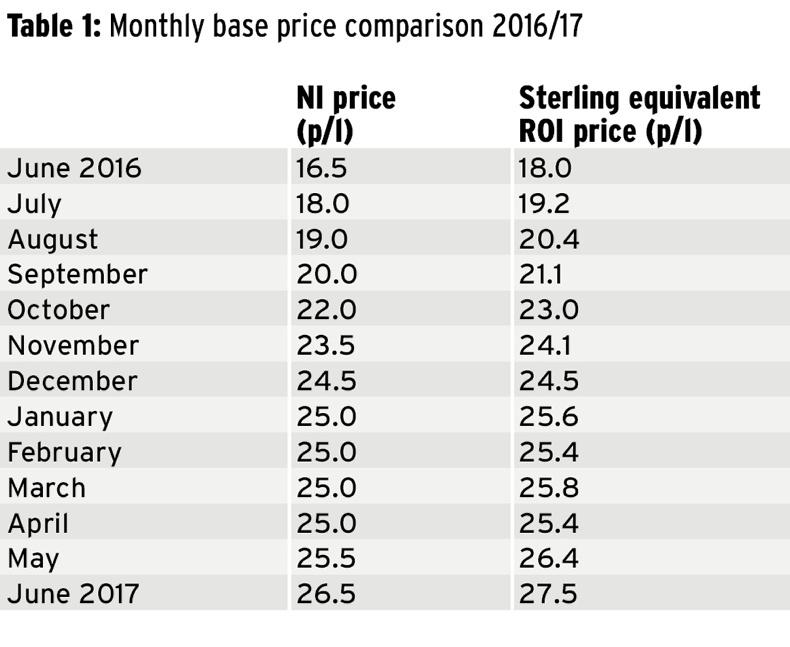

As part of our analysis, we looked at base prices over the last 13 months set by one of these co-ops (Table 1). The Republic of Ireland prices exclude VAT, and all prices are before any adjustments for quality or volume. It should also be noted that these prices do not allow for winter bonuses, which can be worth anywhere between 1p/l and 3p/l over winter months. The exchange rate used to convert to sterling was that prevailing at the time.

Table 1 shows that the gap in base prices is wider now than it has been at any point in 2017. Over the last 13 months, the monthly difference averages just over 0.8p/l. Even allowing for winter bonuses, the analysis suggests that slightly less has been paid as a base price to farmers in NI than counterparts in the south. Producers here will also point to the flat production profile in NI and savings being realised in transport costs given that the amount of milk produced on the average dairy farm in NI is over twice that in the Republic of Ireland.

SHARING OPTIONS