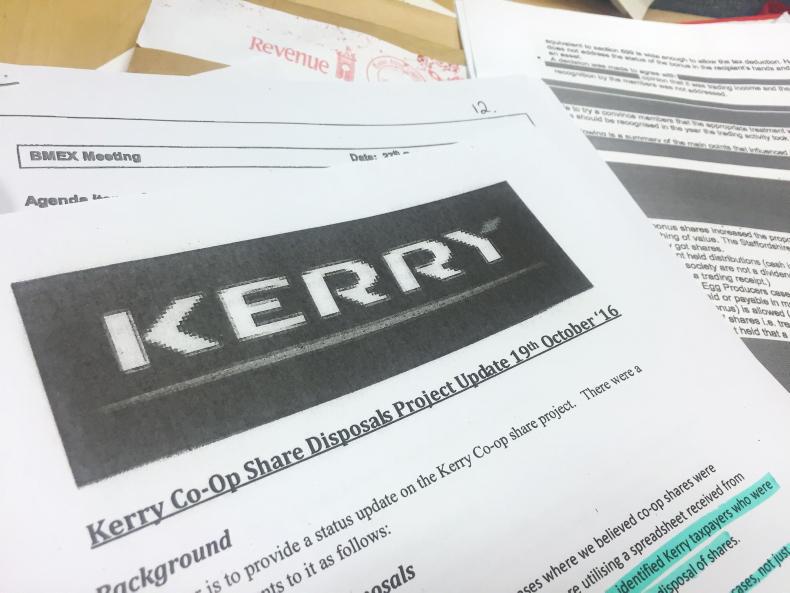

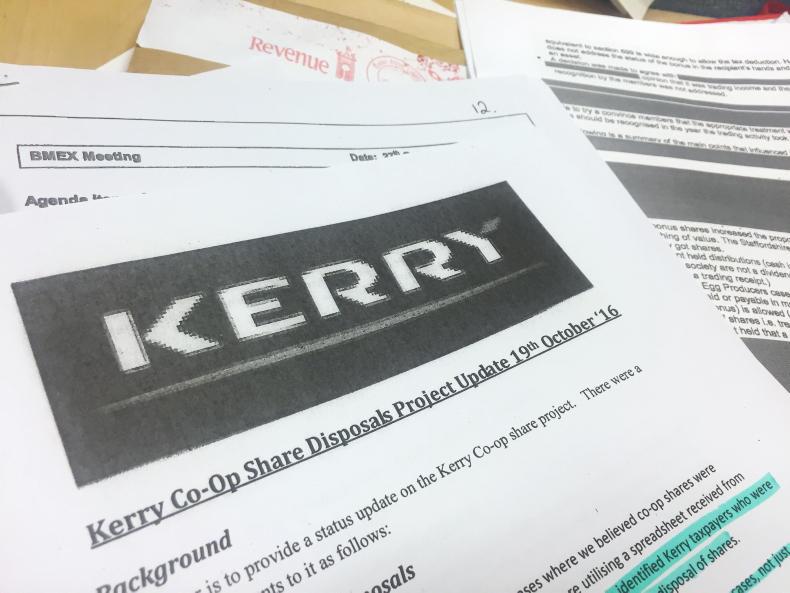

According to instructions circulated to Revenue personnel on 22 and 23 November, the internal manual used as reference by staff conducting tax audits was “updated” to reflect the stance adopted on Kerry patronage shares.

The section dedicated to share issues by co-ops includes a new section indicating that all co-op shares issued “where the amount of shares issued is dependent on the level of business between the member or the co-operative, and where the shares are issued at less than market value, then Revenue will regard the difference between the subscription amount and the market value of the shares (known as “patronage shares”) at the date of issue as a profit of the business of the member”.

This is presented as an exception to the general rules governing co-op spin-outs, which until then advised share swaps “will not be treated as a distribution” and referred to capital gains tax only.

Listen to a discussion of the Revenue's Kerry co-op project in our podcast below:

Listen to "Inside the Revenue's Kerry co-op project" on Spreaker.

Exposed: Revenue’s Kerry co-op project

3,500 Kerry suppliers to get tax bills this year

Only 128 share sales over seven years

The people at the centre of Kerry shares project

More than €400,000 in tax already recouped from Kerry Co-op shareholders

Revenue knew Kerry suppliers were 'broke' as it sent tax claims

Revenue may target 2013 Kerry spin-out

SHARING OPTIONS