The prices paid for milk in NI might be below the EU average, but over the last 12 months they have still increased by 53% or 9.9p/l.

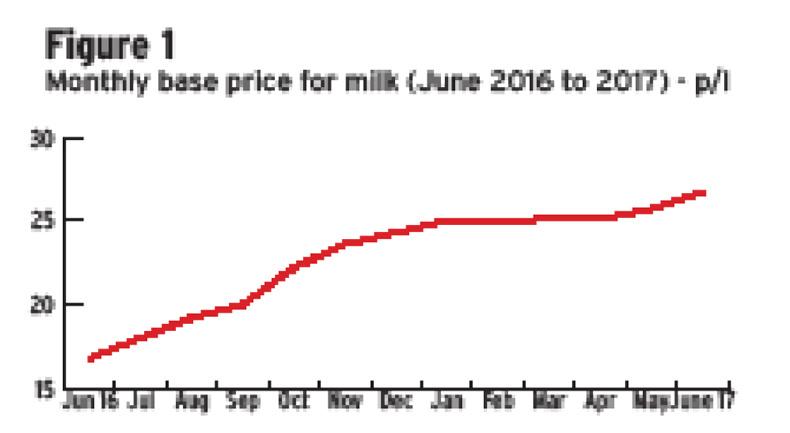

Base prices averaged 26.7p/l for June 2017 compared with 16.8p/l across all processors back in June 2016. This means a 1m-litre producer who supplied approximately 100,000 litres during the month of June in both calendar years saw an additional income of £9,900 in the June 2017 milk cheque.

While the increased income will be welcome, it must be remembered that there was a significant increase in borrowings to fund dairy farms during the downturn, that, in many cases, have yet to be repaid.

Approximately £87m of additional borrowings were loaned to the dairy sector over 2015 and the first half of 2016.

Improving commodity markets, especially for butterfat, and incentives to reduce production within key dairy -roducing regions, have seen milk prices rising month on month since June 2016.

Figure 1 highlights the trend in monthly base price. Prices stalled during spring 2017 as there was a challenging period when Global Dairy Trade (GDT) auctions were under price pressure, especially for milk powders which brought a reopening of EU intervention stores. However, since mid-March there has been upward momentum in demand for whole milk and skim powder. Dairy markets remain finely balanced, with demand for butterfat the key driver in the current trend of rising prices.

The average milk price paid in NI in the period from June 2016 to May 2017 was 23.82p/l. This compares with 19.2p/l for the 12-month period ending May 2016, and is worth an additional £46,000 in income for a 1m litre producer.

Britain

The recovery in global dairy markets has also brought rising prices in Britain. Average price paid there has increased from 20.5p/l in June 2016 to 26.86p/l by May 2017. The average over the period is 24.87p/l, up from 23.9p/l for the 12 months ending May 2016.

SHARING OPTIONS