PRSI changes

I am referring to your article in Irish Country Living, dated 16 August, 2014, “PRSI – pay now to benefit later”. My wife took voluntary redundancy last year, after 30 years of full-time employment, and is now helping me on the farm. The article referred to above states that if I pay her at least €5,000 of self-employed income on the tax return for 2014, she will receive 52 Pay Related Social Insurance (PRSI) contributions for the year. It also states that on the tax side, if we are earning over €41,800, it is beneficial to allocate income above this to her for tax purposes. However, the article also states that Declan McEvoy of IFAC is clear that there is no benefit to paying your wife a wage to reduce tax, especially now, as it would rule her out of making PRSI contributions. The reason for this is that a partner employed by their self-employed spouse is still not allowed to pay PRSI on that income. Please clarify.

The main point to understand about the change to the PRSI situation is to know the difference between paying a wage to a spouse and allocating self-employed income. You are right in that partners employed by spouses (getting a wage) are still not allowed to make PRSI contributions. However, the changes implemented earlier in the year mean that if you allocated self-employed farm income to your spouse, she will be eligible to pay PRSI contributions. It has to be a minimum of €5,000. Remember, it is not automatic and she has to pay a minimum of €500 in PRSI contributions to actually get them.

On the issue of if you are earning over €41,800 is it beneficial to allocate income to her, this comes from the fact that couples with two incomes only maximise their low-rate tax bands when the first income is over €41,800 and the second income is over €23,500. Hope this clarifies the issue.

Fair deal scheme

My husband inherited half of a farm from his sister six months ago. His sister had a bad fall two months ago and is in a nursing home. My husband continues to run the farm for her, he also farms his own. How does he stand with the Fair Deal Scheme, will we be hit by the asset contribution of 7.5%?

Firstly, it is your husband’s sister that will be hit by any asset contribution, not your husband. As explained last week, the HSE will only make contract with the person entering a nursing home. The farm is taken into account in the financial assessment of assets, ie a charge of 7.5% per annum.

The fact that the land was only transferred six months ago means that all of the land could be counted, even the land that was transferred. However, in certain circumstances, a three-year limit similar to the situation with a principal residence, where the charge is capped at 22.5% (ie payable for at 7.5% per year for the first three years in care only), can be applied.

The first is where the person has suffered a sudden illness or disability which causes them to require long-term residential care. This is the case in your situation.

The second is where the person or their partner was actively engaged in the daily management of the farm, or relevant business, up until the time of the sudden illness or disability. This again was the case in your situation.

Finally, a family successor has to certify that he or she will continue the management of the farm or relevant business.

According to the Nursing Home Support Scheme Act 2009, a family successor means “a partner or relative of the person applying for State support, which person, at the time of the application for State support… in the case of a farm, regularly and consistently applies a portion of his or her working day in farming the farm”.

Based on this, your husband would qualify. It would appear that the non-transferred part could have a three-year cap applied. The problem is that bizarrely enough it would appear that her transferred asset could be indefinitely counted against her estate, unless your husband pays for her care for the next four and a half years upfront. Your situation highlights an anomaly in the scheme, where people are at a disadvantage by handing over the farm if they end up in a nursing home within five years. It is worth looking into further.

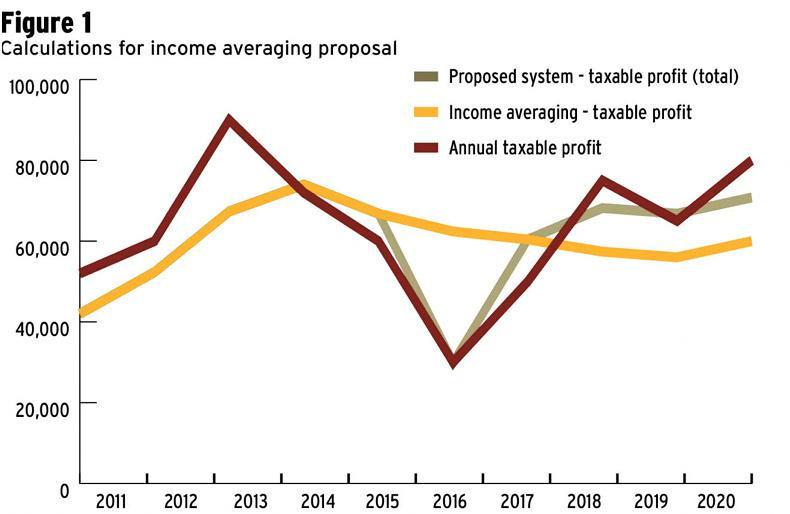

Income averaging

I rear my own calves and sold a lot of stock in December 2013. It was only when I went to my accountant that I realised it left me exposed to a large tax bill this year. I asked my accountant about income averaging, but he said that because my wife works four days a week in a crèche I’m not eligible. Is there anything I can do?

As you rear your own stock, the animals were most likely in at a low book value on 1 January 2013 and that increased your profits on paper. It will be lower next year, but that is not much good to your cashflow now and shows the importance of tax planning, especially when selling stock around your year end.

Income averaging would be a big help. You say your wife works in a crèche for four days a week. If she is just employed and does not own the business then you should not be ruled out of income averaging for that reason.

Revenue clearly states that only farmers who, or whose spouses, carry on another trade or profession cannot opt for income averaging. You are also ruled out if you are a director of a company which carries on a trade or profession. Go back to your accountant to make sure. With income averaging moving to five years in 2015, it will be even more beneficial to farmers.

SHARING OPTIONS