The Irish cattle sector is characterised by two distinct farm types – rearing farms, which are those with suckler cows, and fattening or finishing farms, which typically purchase store animals for finish.

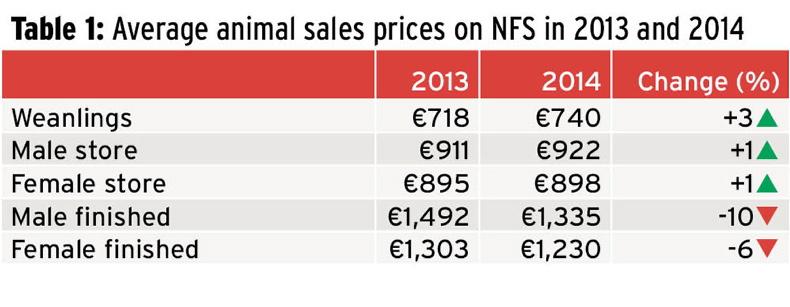

These two farm types had contrasting results last year. Prices for younger animals increased in the 2014 calendar year compared with 2013, while prices for finished animals declined. Beef finishers had to endure a 20% reduction in output value compared with 2013. This is unsurprising given the beef price crisis of 2014.

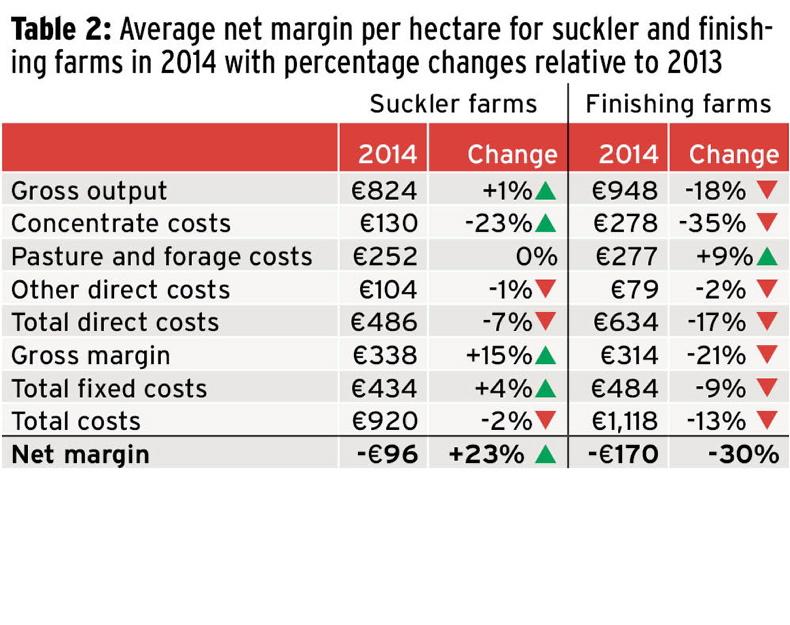

In general, the gross output/ha on suckler farms was more or less unchanged from 2013 to 2014, with those selling young stock typically doing better.

The value of output on cattle-finishing farms was down almost 20% as a result of negative price movements for finished animals, lower production levels and higher purchase prices for young animals.

In general, direct costs of production on cattle farms decreased in 2014 relative to the previous year, largely due to a reduction in feed bills following a recovery from the fodder crisis of 2013.

Negative

Nevertheless, neither of the cattle enterprises managed to produce a positive net margin before decoupled direct payments are considered. The negative net margin on the average cattle finishing farm deteriorated by a further 30%, bringing margins to an average loss of €170/ha.

Overall, the profitability of suckler farms improved with the negative net margin on suckling farms declining to a loss of €96/ha compared with a loss of €123/ha in 2013.

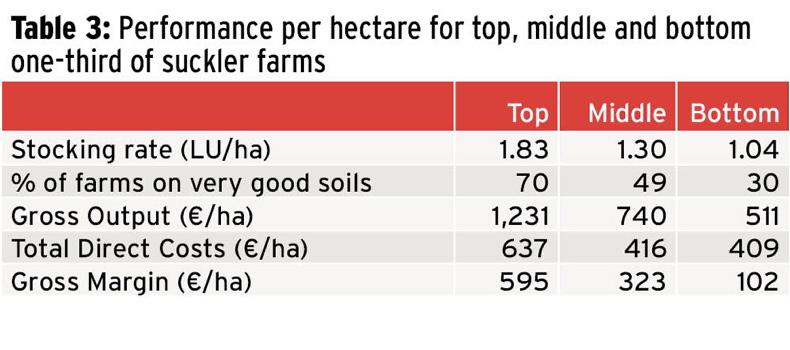

Output, costs of production and profit per hectare vary substantially across cattle farms. Table 3 presents the performance for suckler farms. There is more than a fivefold difference in the gross margin per hectare earned by the top one-third of farms relative to the bottom one-third. This is driven by higher output and lower costs on the better-performing farms. However, the natural advantage of the top one-third should be noted, with 70% of them on very good soils compared with only 30% of the bottom group.

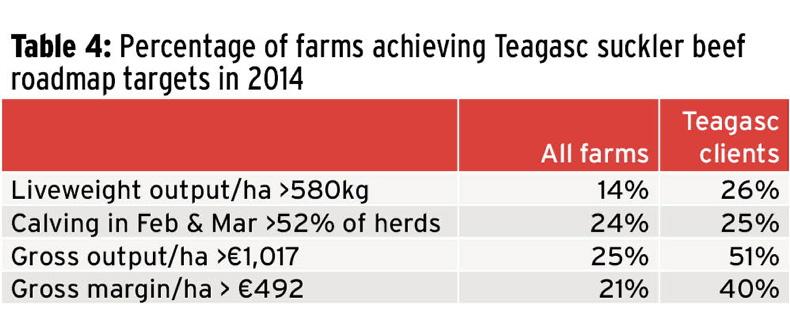

The Teagasc roadmap presents key performance targets for suckler farms to achieve by 2025.

While there is a clear relationship between soil quality and technical performance, Table 4 illustrates the role of knowledge and advice in enhancing productivity and profit. Teagasc clients were more likely to have achieved these roadmap targets last year.

One of the key targets in the Teagasc beef roadmap is to increase output per hectare to levels greater than 580kg by 2025.

In 2014, 14% of farms were already achieving this target and 26% of Teagasc clients. Similarly, Teagasc clients were also more likely to achieve the compact calving target.

Most importantly, the role of knowledge and advice in enhancing productivity and profit is evident, with Teagasc clients being more likely to achieve the output and gross margin per hectare targets.

Clearly 2014 was a challenging year for cattle-finishing farms, with significant reductions in profit margins. In 2015, it seems a reversal of this negative price movement is likely.

But regardless of how the beef meat market develops over the remainder of 2015, which is beyond the control of the individual farmer, it is clear that farmers participating in knowledge transfer programmes with Teagasc perform better than those who do not.

SHARING OPTIONS