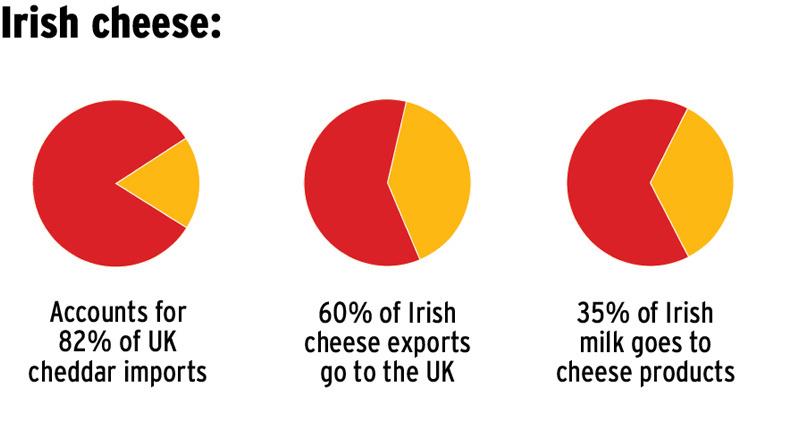

A hard Brexit scenario with World Trade Organisation (WTO) tariffs will put the equivalent cost of 16c/l on to milk directed to cheese destined for the UK market – a bill of €150m annually for the industry. This will make it unviable for Ireland, which exports 60% of its cheese production to the UK.

The UK’s response may be to import its cheese from third countries under free trade agreements or produce it internally. Meanwhile, the Irish dairy industry, which has invested in cheese capacity to prepare for the post-quota scenario, may see some of its cheese factories mothballed.

In 2016, almost 40% of Ireland’s milk went to make 210,000t of cheese, where just over 20% of Ireland’s milk pool went to make cheese for the UK.

In 2016, the UK imported 96,000t of cheddar cheese, 5% less than in 2015. Ireland was the dominant source, accounting for 82% of these imports, followed by France and Germany. This January, cheddar cheese imports to the UK fell 13% compared with the same month last year. Imports from Ireland were down 10,300t (12%).

We should not be fooled into thinking the British people will stop eating cheese. The declining level of imports has come as a direct result of UK cheddar production hitting record highs. In spite of lower volumes of manufacturing milk being produced, key UK processors strategically focused on the output of cheese, with total production reaching almost 212,000t, a 3% year-on-year increase.

Alternatively, to keep cheese affordable to its people, the UK Government could negotiate a free trade agreement with the likes of the US or New Zealand, both among the fastest-growing cheese exporters since 2011, with the US up 43% and New Zealand up 7.5%.

Both these scenarios are a cause for concern. The direct impact will be that some 1.3bn litres of milk will need to find a new home, either as cheese or as alternative products.

But as the Europeans don’t necessarily eat cheddar, and with limited opportunities around speciality cheese, will the only real alternative be to move an increasing proportion of the Irish milk pool to dairy powders?

This has already been the case with Dairygold, which has seen 65% of its extra milk move to powders since 2014. A hard Brexit scenario could escalate this for the industry. If this is the case, before individual co-ops move to take individual decisions, should the industry discuss again dairy processing across the island that reduces risk for the milk pool and maximises the farmer’s return on investment as a whole?

Who makes Ireland’s cheese

Ireland makes around 180,000t of cheddar and around 30,000t of speciality cheeses, such as brie and mozzarella. The majority of this is concentrated with four processors.

Glanbia now has the capacity to produce almost 90,000t after it announced a €35m investment to double capacity to 40,000t at its Wexford site last year, to complement its Ballyragget cheese facilities.

Dairygold has the capacity at Mitchelstown to produce 50,000t. Kerry has around 40,000t of capacity at its Newmarket facility, while Carbery has 50,000t of capacity at Balineen.

SHARING OPTIONS