Live cattle exports play a crucial role in Irish cattle production. Ireland has always been well-known for its high exports of good-quality live cattle.

However, in the past few years, fluctuations in live cattle prices in Ireland, compared with our neighbours across the water and in continental Europe, have seen the number of cattle exported from Ireland vary considerably.

In fact, live export numbers can be seen to have become cyclical in recent years. Periods of low cattle prices have resulted in high levels of exports, while periods of high prices have resulted in low export levels.

Peaks and troughs

As we know, there is a fine line between demand and supply. Although beef factories have grown exports in recent years to cope with rising supply of cattle, when supply is greater than demand, prices fall quickly.

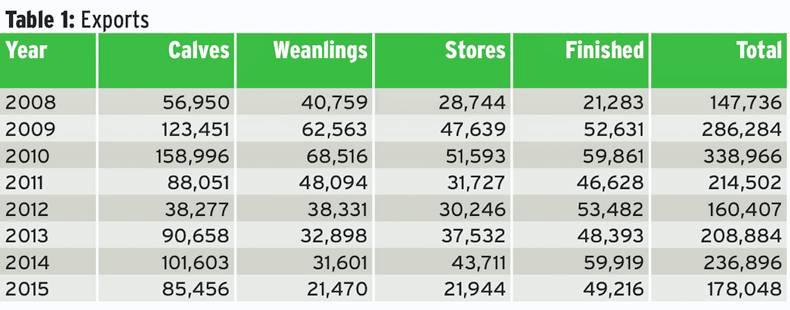

Table 1 details the numbers exported in recent years. Looking at 2008, slightly higher live prices resulted in low exports. As live cattle prices fell in 2009 and 2010, the numbers exported increased. Beef price and live cattle prices improved in 2012, resulting in a strong trade and reduced exports. This had a knock-on effect running into 2013 and 2014, as higher supplies, combined with an increasing kill of young bulls, resulted in a difficult beef trade for 2014.

Extremely strong live prices last year had a similar effect as in 2012, cattle exports fell by about 58,850 head.

At the same time, calf births increased by over 119,000 head. Combined with a weaker beef price, this has started to have an effect on the price paid for weanlings and store cattle.

With prices falling slightly, exporters are expecting to be able to move more numbers this year, with peak continental weanling exports expected in the autumn.

Calf exports to rise

It is widely anticipated that calf exports will rise this year. With just 85,000 head exported last year, strong demand from the Spanish market, combined with steady demand from the Dutch market, should keep a solid floor under calf exports.

Again, the price point is critical. While strong calf exports will not directly affect suckler farmers, having less of these cattle available in the domestic market will be beneficial.

Last year saw a strong increase in demand for Angus and Hereford calves from the dairy herd.

In many cases, these will be brought to beef, but the Beef Data Genomics Programme (BDGP) scheme could also see an increase in demand for these dairy-cross animals as five-star replacements for the suckler herd.

Alan Kelly looks at this more closely at this

With the cost of exporting a weanling to Italy running at about €120 to €150/head, when all costs are taken into account a differential needs to be in place for exports to be feasible.

At the end of the first week of January, Bord Bia figures show the average Irish weanling price to be €2.36/kg excluding VAT.

Bear in mind that this is the average price of weanlings in Ireland, not the average price of export-quality weanlings.

In Spain, the equivalent crossbred was making €2.70/kg, while in France the average price was €2.55/kg.

More boats approved

North Africa has attracted growing numbers of Irish cattle since the re-opening of the markets. Libya, Morocco and Tunisia have been the main export destinations in the past few years.

This week, the Department of Agriculture has confirmed that three ships are currently in the process of being approved to export livestock abroad. This will dramatically increase the capacity for exports throughout 2016.

It is understood the Department is working with Bord Bia and some Irish exporters to further increase export opportunities for Irish cattle.

Speaking in the Dáil this week, Minister Simon Coveney said: “My department is currently investigating the possibilities for agreeing bilateral health certificates for the export of fattening and slaughter cattle to Egypt and Algeria, and breeding cattle to Kazakhstan, Morocco, Algeria and Turkey.”

Action on barriers to NI and UK

Despite inroads being made into export markets across Europe and north Africa, there remains barriers to the UK market. In the first few weeks of the year, the number of finished cattle going north for slaughter has increased.

However, mart managers continue to say that northern buyer activity at marts in the south is low to non-existent, despite there being a large differential between cattle prices north and south of the border.

The same can be said for the UK. There are only a handful of feeders sourcing cattle in Ireland for finishing in the UK.

These are generally finishers supplying wholesale-type factories. Strong barriers remain in place against significant numbers of cheaper Irish cattle moving north, or across the water to the UK.

Processors have given clear signals on their stance. They have outlined that cattle born in Ireland and finished in the UK must be boned out separately from UK-born and finished cattle.

In addition, there are marketing issues regarding Irish born UK finished animals.

Under country of origin labelling, this beef has no identity and this acts as a barrier to trade.

While exports in 2016 are looking more positive than last year, the industry as a whole needs to examine live cattle price and export trends. Price volatility is not in farmers’ interests, as it leaves it hard to plan financially.

In addition, the fluctuations in prices can have a negative impact on exporters. Steadier prices help to copperfasten export links, so that buyers return year-on-year.

Opening up exports to the UK is essential. Regardless of the road blocks which exist, there are major issues around market access which need addressing.

To read the full Suckler Focus Supplement click here.

{kind=link}

SHARING OPTIONS