International grain markets ended 2016 in a similar vein to how they performed for the past number of months – low and volatile. It is almost as though the markets realise there is no future down at this low base driven by high supply and they are trading on every scrap of news that has the potential to take them up a notch. But they are always beaten back by the sheer weight of surplus, even though much of it is actually not available to the market by virtue of politics of location.

The major uncertainties for the moment are maize and soya bean outputs in South America. It is at least possible that the high output levels predicted earlier may not come to pass due to concerns over increasing dryness. While reduced output from this region would have little impact on current prices, reduced production there would increase the seriousness of other weather-related problems that could occur elsewhere in the world in the coming year.

Meanwhile, oilseed prices remain quite strong to keep the option open for this crop for 2017. And soya bean has dropped from its recent highs of $10.7/bu to just over $10/bu as this market also trades in weather news and grower intentions.

ADVERTISEMENT

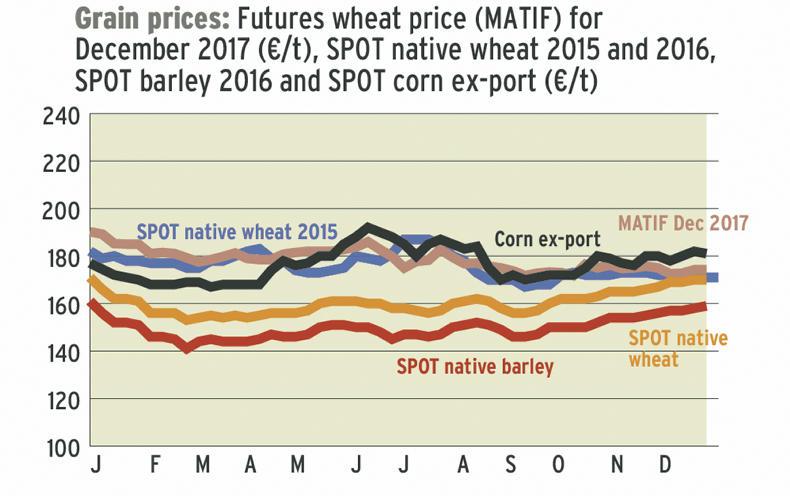

Native prices remain broadly similar to how they ended 2016. Spot wheat is around €170/t with barley at €159 to €160/t. Prices for March/May still range around €173 to €174/t, with barley at €162 to €163/t. New-crop wheat price remains around €170/t, with barley around €160/t.

This content is available to digital subscribers and loyalty code users only. Sign in to your account, use the code or subscribe to get unlimited access.

The reader loyalty code gives you full access to the site from when you enter it until the following Wednesday at 9pm. Find your unique code on the back page of Irish Country Living every week.

CODE ACCEPTED

You have full access to the site until next Wednesday at 9pm.

CODE NOT VALID

Please try again or contact support.

International grain markets ended 2016 in a similar vein to how they performed for the past number of months – low and volatile. It is almost as though the markets realise there is no future down at this low base driven by high supply and they are trading on every scrap of news that has the potential to take them up a notch. But they are always beaten back by the sheer weight of surplus, even though much of it is actually not available to the market by virtue of politics of location.

The major uncertainties for the moment are maize and soya bean outputs in South America. It is at least possible that the high output levels predicted earlier may not come to pass due to concerns over increasing dryness. While reduced output from this region would have little impact on current prices, reduced production there would increase the seriousness of other weather-related problems that could occur elsewhere in the world in the coming year.

Meanwhile, oilseed prices remain quite strong to keep the option open for this crop for 2017. And soya bean has dropped from its recent highs of $10.7/bu to just over $10/bu as this market also trades in weather news and grower intentions.

Native prices remain broadly similar to how they ended 2016. Spot wheat is around €170/t with barley at €159 to €160/t. Prices for March/May still range around €173 to €174/t, with barley at €162 to €163/t. New-crop wheat price remains around €170/t, with barley around €160/t.

If you would like to speak to a member of our team, please call us on 01-4199525.

Link sent to your email address

We have sent an email to your address. Please click on the link in this email to reset your password. If you can't find it in your inbox, please check your spam folder. If you can't find the email, please call us on 01-4199525.

ENTER YOUR LOYALTY CODE:

The reader loyalty code gives you full access to the site from when you enter it until the following Wednesday at 9pm. Find your unique code on the back page of Irish Country Living every week.

SHARING OPTIONS