Global grain prices had another up and down week on the back of stock levels and increased supply estimates. Currency has again been a big factor as it affected Russian and euro prices in particular.

News of continuing strong corn exports from the US was one of the supports in the past week and it helped to counterbalance the increasingly large South American maize harvest.

ADVERTISEMENT

Egypt was back in the market again last week and purchased 420,000t of mainly central European origin wheat but some French also. It is the biggest importer of wheat and some believe that its overall demand is increasing.

Wheat markets in the US were helped by ongoing concerns over dryness in the wheat belt and this helped futures last week. However, this appeared to be reversing again.

Meanwhile, Chicago soya bean futures have continued to weaken since the start of March on the back of high South American output and an expected increase in the area to be planted in the US this spring. This has also affected EU rape prices.

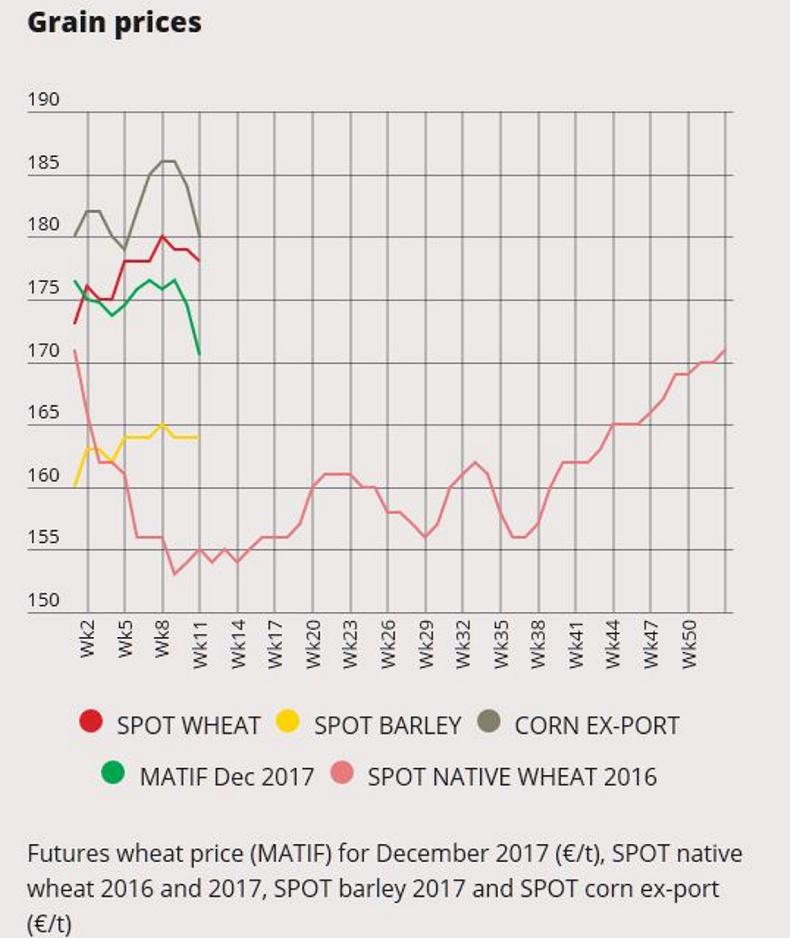

But physical markets remain largely stubborn, as there are relatively few sellers in the market currently. Native spot prices have a slightly weaker tone, with wheat at €177 to €178/t and barley at €163 to €165/t. May prices are slightly stronger at €179 to €181/t for wheat and €164 to €166/t for barley. However, June/July wheat might make €180 to €182/t. November wheat is quoted at €170 to €172/t with barley at €160 to €162/t.

Register for free to read this story and our free stories.

This content is available to digital subscribers and loyalty code users only. Sign in to your account, use the code or subscribe to get unlimited access.

The reader loyalty code gives you full access to the site from when you enter it until the following Wednesday at 9pm. Find your unique code on the back page of Irish Country Living every week.

CODE ACCEPTED

You have full access to the site until next Wednesday at 9pm.

CODE NOT VALID

Please try again or contact support.

Global grain prices had another up and down week on the back of stock levels and increased supply estimates. Currency has again been a big factor as it affected Russian and euro prices in particular.

News of continuing strong corn exports from the US was one of the supports in the past week and it helped to counterbalance the increasingly large South American maize harvest.

Egypt was back in the market again last week and purchased 420,000t of mainly central European origin wheat but some French also. It is the biggest importer of wheat and some believe that its overall demand is increasing.

Wheat markets in the US were helped by ongoing concerns over dryness in the wheat belt and this helped futures last week. However, this appeared to be reversing again.

Meanwhile, Chicago soya bean futures have continued to weaken since the start of March on the back of high South American output and an expected increase in the area to be planted in the US this spring. This has also affected EU rape prices.

But physical markets remain largely stubborn, as there are relatively few sellers in the market currently. Native spot prices have a slightly weaker tone, with wheat at €177 to €178/t and barley at €163 to €165/t. May prices are slightly stronger at €179 to €181/t for wheat and €164 to €166/t for barley. However, June/July wheat might make €180 to €182/t. November wheat is quoted at €170 to €172/t with barley at €160 to €162/t.

If you would like to speak to a member of our team, please call us on 01-4199525.

Link sent to your email address

We have sent an email to your address. Please click on the link in this email to reset your password. If you can't find it in your inbox, please check your spam folder. If you can't find the email, please call us on 01-4199525.

ENTER YOUR LOYALTY CODE:

The reader loyalty code gives you full access to the site from when you enter it until the following Wednesday at 9pm. Find your unique code on the back page of Irish Country Living every week.

SHARING OPTIONS