What is truly remarkable about the Irish forest sector is its imminent growth projections. Over the next 10 to 15 years, the output from Irish forests is forecast to double, potentially stimulating a further 10,000 jobs and contributing a further €2bn of economic activity, all deeply rooted in the hard-pressed rural economy.

We are fortunate to have a world-class, export-focused timber processing sector that has the physical, technological and intellectual capacity to drive this growth opportunity and capture this additional value.

This significant opportunity, however, is heavily dependent on one factor more than any other: continued access to the UK market. The UK is, by some distance, the largest importer of timber in Europe and currently consumes over 75% of Irish timber.

Impact of Brexit

No one knows what the precise impact of Brexit will be on Ireland. There is, however, broad agreement that:

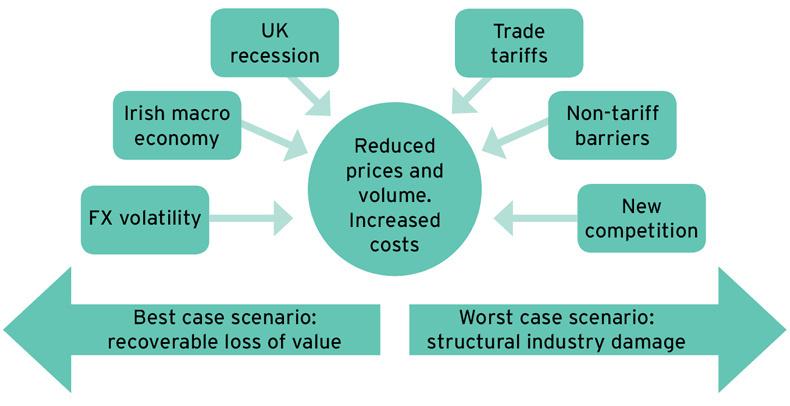

It will be unambiguously negative for Irish consumers and producers.Its impact will be felt most acutely in the rural Ireland. Similarly, no one knows what the scale of the impact of Brexit will be on the timber industry. The immediate impact is dominated by foreign exchange currency volatility and increasing levels of uncertainty. As for all exporters to the UK, Irish timber has been hit hard by the devaluation of sterling. The immediate reduction in value of circa 15% and consequent reduction in end-market prices has flowed upstream through the supply chain to growers and contractors.

Once the UK triggers Article 50, levels of uncertainty are likely to increase, bringing new risks to the UK and Irish economies, specifically in the construction sector, as industry defers key investment decisions, potentially reducing the demand for Irish timber products.

Thankfully, the spectre of enormous trade tariffs is not likely to apply to sawn timber. Sawn coniferous timber currently attracts a tariff of 0% under existing World Trade Organisation (WTO) rules. But wood panels such as Medite and SmartPly, which are the major consumers of pulpwood from forest thinning in Ireland, would attract a tariff of 7% if WTO rules are applied. Such a tariff essentially translates directly as an additional cost for the exporter and is likely to be passed back to growers in terms of reduced prices.

Non-tariff costs

A key feature of the single market has been the minimising of non-tariff barriers. If the UK leaves the customs union, as now seems inevitable, there will be a significant increase in such barriers to trading with the UK. These could include customs controls, additional documentation, different labelling and packaging as well as different VAT declarations. New storage facilities and distribution centres may need to be constructed at key transit points.

Due to its high volume-to-value ratio, transport and logistics form a significant element of cost in the timber supply chain. Any increase in cost per load has a disproportionately high impact on the costs of getting the timber to its market. More worryingly, these barriers may remove one of the few competitive advantages that Irish timber has in the UK: the ability to deliver a load of timber to the end user quicker than any other timber exporter.

As the UK starts to put in place free trade agreements with other countries, it is possible that we will see new competition emerging. With increasing trade tensions between Canada and the US, it is feasible that bulk shipments of Canadian timber could start to arrive in UK ports as in the past.

Since the decision to leave the EU, the UK economy has remained fairly buoyant and the volume of Irish timber being imported has remained relatively strong. As Brexit progresses, however, the signposts are all pointing towards reduced prices, increased costs and potentially lower volumes. When all of this is combined, the best scenario we could hope for would be a temporary, but recoverable, loss of value from the industry. A worst case scenario, however, could result in structural industry damage setting it on an irreversible path of contraction rather than growth.

Having survived the economic crash in 2007, the timber industry has learned some real resilience. It is lean and efficient and will face Brexit determined to deliver growth opportunities for rural Ireland.

Bill Stanley is director of strategy and new business, Coillte Read more

Focus: Forestry & chainsaws

What is truly remarkable about the Irish forest sector is its imminent growth projections. Over the next 10 to 15 years, the output from Irish forests is forecast to double, potentially stimulating a further 10,000 jobs and contributing a further €2bn of economic activity, all deeply rooted in the hard-pressed rural economy.

We are fortunate to have a world-class, export-focused timber processing sector that has the physical, technological and intellectual capacity to drive this growth opportunity and capture this additional value.

This significant opportunity, however, is heavily dependent on one factor more than any other: continued access to the UK market. The UK is, by some distance, the largest importer of timber in Europe and currently consumes over 75% of Irish timber.

Impact of Brexit

No one knows what the precise impact of Brexit will be on Ireland. There is, however, broad agreement that:

It will be unambiguously negative for Irish consumers and producers.Its impact will be felt most acutely in the rural Ireland. Similarly, no one knows what the scale of the impact of Brexit will be on the timber industry. The immediate impact is dominated by foreign exchange currency volatility and increasing levels of uncertainty. As for all exporters to the UK, Irish timber has been hit hard by the devaluation of sterling. The immediate reduction in value of circa 15% and consequent reduction in end-market prices has flowed upstream through the supply chain to growers and contractors.

Once the UK triggers Article 50, levels of uncertainty are likely to increase, bringing new risks to the UK and Irish economies, specifically in the construction sector, as industry defers key investment decisions, potentially reducing the demand for Irish timber products.

Thankfully, the spectre of enormous trade tariffs is not likely to apply to sawn timber. Sawn coniferous timber currently attracts a tariff of 0% under existing World Trade Organisation (WTO) rules. But wood panels such as Medite and SmartPly, which are the major consumers of pulpwood from forest thinning in Ireland, would attract a tariff of 7% if WTO rules are applied. Such a tariff essentially translates directly as an additional cost for the exporter and is likely to be passed back to growers in terms of reduced prices.

Non-tariff costs

A key feature of the single market has been the minimising of non-tariff barriers. If the UK leaves the customs union, as now seems inevitable, there will be a significant increase in such barriers to trading with the UK. These could include customs controls, additional documentation, different labelling and packaging as well as different VAT declarations. New storage facilities and distribution centres may need to be constructed at key transit points.

Due to its high volume-to-value ratio, transport and logistics form a significant element of cost in the timber supply chain. Any increase in cost per load has a disproportionately high impact on the costs of getting the timber to its market. More worryingly, these barriers may remove one of the few competitive advantages that Irish timber has in the UK: the ability to deliver a load of timber to the end user quicker than any other timber exporter.

As the UK starts to put in place free trade agreements with other countries, it is possible that we will see new competition emerging. With increasing trade tensions between Canada and the US, it is feasible that bulk shipments of Canadian timber could start to arrive in UK ports as in the past.

Since the decision to leave the EU, the UK economy has remained fairly buoyant and the volume of Irish timber being imported has remained relatively strong. As Brexit progresses, however, the signposts are all pointing towards reduced prices, increased costs and potentially lower volumes. When all of this is combined, the best scenario we could hope for would be a temporary, but recoverable, loss of value from the industry. A worst case scenario, however, could result in structural industry damage setting it on an irreversible path of contraction rather than growth.

Having survived the economic crash in 2007, the timber industry has learned some real resilience. It is lean and efficient and will face Brexit determined to deliver growth opportunities for rural Ireland.

Bill Stanley is director of strategy and new business, Coillte Read more

Focus: Forestry & chainsaws

SHARING OPTIONS