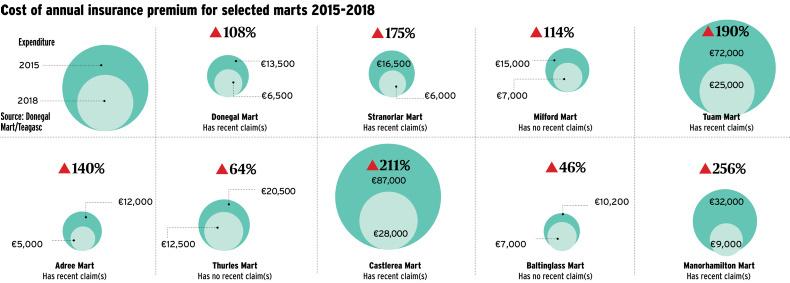

Marts have seen the cost of their insurance premiums rise by 20% to 30% in the past year alone, according to Donegal mart manager Eimear McGuinness, who spoke on behalf of the sector at a recent Oireachtas committee hearing. For some marts, the cost of insurance has tripled in the past three years. “Continued hikes in insurance premiums if unaddressed will bring about mart closures,” McGuinness said. Why is this happening and what can be done?

Problem: excessive injury compensation

“We simply value injury too highly in this country, and I mean soft tissue injury especially,” said FBD Insurance’s chief claims officer Jackie McMahon. According to him, a minor ankle injury costs up to €55,700 in Ireland compared with €12,554 in the UK. McGuinness said a man with “a sore toe” had successfully claimed €13,000 against her mart’s insurance.

Solution: regulation

Earlier this year, the Government approved the recommendations of a working group on the cost of public liability insurance, including considering legislation to cap the amounts awarded to personal injury claimants and ensuring that the amount paid out is the same whether the case goes through the courts or other channels such as the Personal Injuries Assessment Board.

Problem: too many accidents

A serious accident at Mohill Mart in April illustrated the high exposure to public liability in this business. While only the most serious accidents grab headlines, a larger number of smaller claims constantly make their way to insurers, costing thousands of euros.

Solution: safety measures

Since the Mohill accident, a dozen marts have restricted access to different areas of their premises, mostly in the west where suckler-bred cattle pose a greater risk. Measures range from bans on public access to pens to segregated walkways for farmers and animals and overhead skywalks. These, however, are costly and McGuinness has called for a Government support scheme.

Problem: high legal costs

Mart managers complain that insurers accept to pay out questionable claims without fighting them in court. McMahon said this was because of the high legal costs involved, with FBD paying 40% of all its claim costs in additional legal fees. For smaller claims in the district court, legal costs routinely equal the amount to the claimant and it’s cheaper to settle than to fight. “The legal system is slow, it’s archaic and it’s inefficient – every twist and turn in it,” he said.

Solution: legislation

The Government working group’s report suggests a one-month deadline for anyone to make a personal injury claim. This would mean marts would still have access to archived CCTV footage to verify the case. There are also plans to overhaul training and procedures for the courts to become more efficient in dealing with personal injury cases but powerful legal interests are likely to oppose this.

Problem: insurance fraud

FBD estimates that 20% of all claims received are fraudulent, and only half of these are caught.

There are currently little or no consequences for those making fake or exaggerated claims.

Solution: punish fraudsters

The Government plans to make the authors of fraudulent or exaggerated claims liable to pay the legal costs they cause, and to establish a Garda insurance fraud unit funded by insurers.

Lack of competition

Most marts can only get insurance from FBD, with a few of the larger operators using Aviva. Other insurers refuse to enter this market. “The marts currently are loss-making for us,” said FBD’s chief commercial officer John Cahalan, adding that the insurer covered them because they are important to its farmer customers.

Solution: all of the above

Making mart insurance a profitable business for insurers at a cost that marts can afford in the long run will be the only way to attract more competition in offering this crucial service.

SHARING OPTIONS