Question: My parents are in their early sixties and still farming full-time. We run a 60sc suckler and beef farm in Mayo and I’m the only one of their three children involved in the business. We have started discussing succession more seriously, but the conversations quickly become confusing when tax is mentioned. My parents are worried about making a mistake that could leave us with a large tax bill or force land to be sold in future. What are the main tax issues we should understand before making decisions?

Answer: Your family is already ahead of most. Starting these conversations while your parents are in their early sixties and still actively farming gives you real options that families who leave it too late simply do not have. At around €8,000/ac, 60 acres of Mayo farmland is worth close to €480,000.

That is not a figure you can ignore, but it is also not a figure that should cause any panic if the planning is done properly.

There are three main taxes involved. Capital Gains Tax (CGT) can arise when your parents transfer assets during their lifetime and Capital Acquisitions Tax (CAT) applies when a child receives a gift or inheritance, both charged at 33%. Stamp Duty arises on the legal transfer of land, though reliefs can reduce or eliminate that entirely.

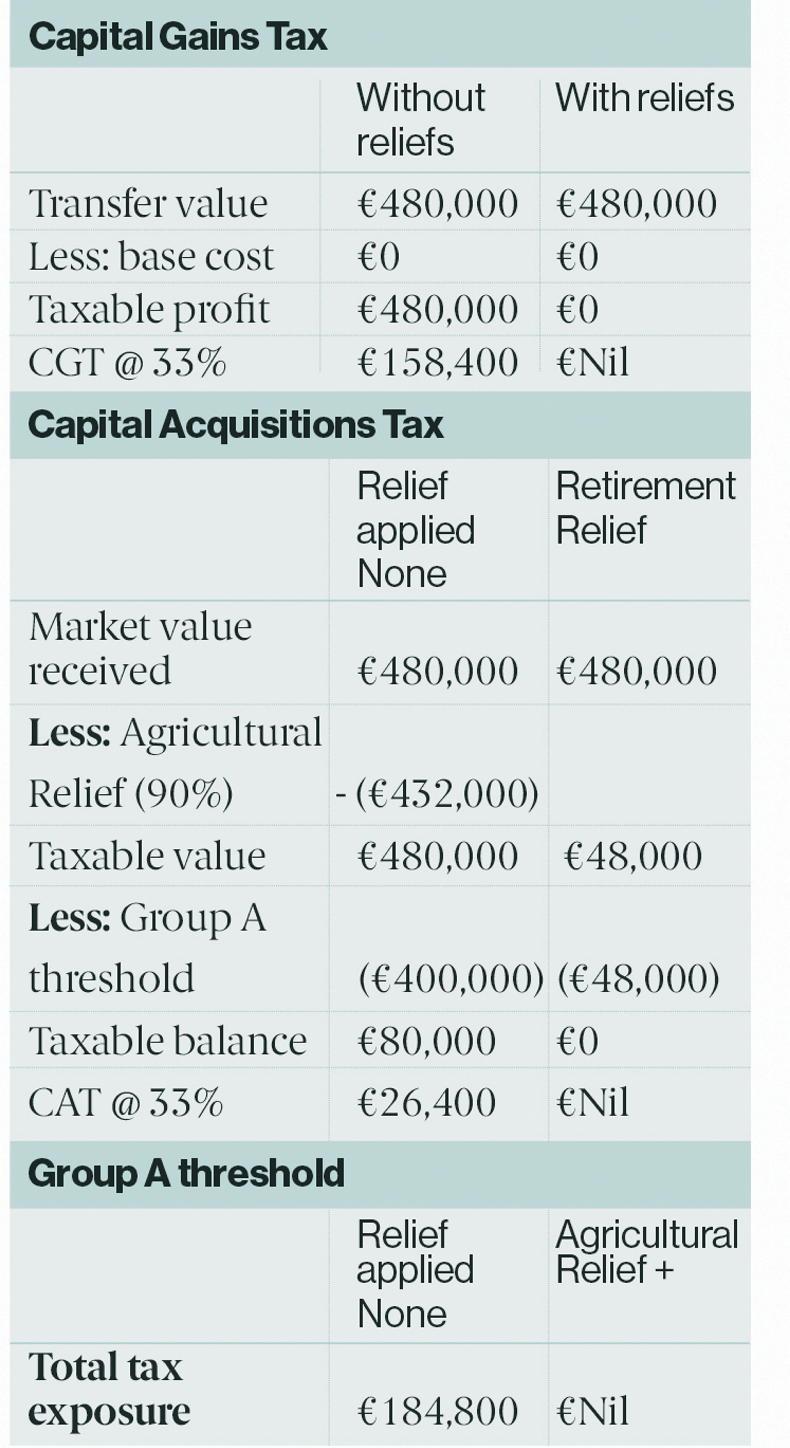

Here is what the numbers look like on a farm valued at €480,000, assuming the land was inherited by your parents and has a negligible base cost. (See Table 1 below)

Retirement Relief

Retirement Relief eliminates the CGT your parents would otherwise pay on transferring the farm to you. The critical point is age, but also history: your parents must have owned and farmed the land for at least 10 years prior to the transfer to qualify.

If your parents transfer while they are between 55 and 69, the relief on a transfer to a child is uncapped – no CGT regardless of the value transferred. If they wait until 70 or beyond, a €3m cap applies, which would still cover this farm comfortably.

Agricultural Relief can reduce the taxable value of farmland by 90%, but strict conditions apply. You must qualify as an active farmer, either through farming qualifications such as the Green Cert or by spending most of your working time farming. You must also satisfy the 80% agricultural asset test.

If you already own significant non-farm assets, like a home in town or a rental property, you could ‘fail’ this test and lose the 90% reduction entirely.

This is your condition to meet, not your parents’, and it needs to be confirmed before any transfer takes place, not assumed.

If it is not met, the €432,000 reduction in the table above disappears.

On Stamp Duty, the numbers tell their own story.

Consanguinity rate with Young Trained Farmer Relief

Transfer value: €480,000/€480,000

Stamp Duty rate: 1%/0%

Stamp Duty payable: €4,800/€Nil

Stamp Duty may also arise, but reliefs are more straightforward. Young Trained Farmer Relief can reduce Stamp Duty to nil where the child is under 35 and holds the required qualification. Otherwise, the 1% family transfer rate generally applies between parent and child.

The question of your siblings is the one that most families find difficult. A 60ac suckler farm does not divide three ways without breaking something. Many families instead use other assets, such as savings, life assurance or the family home, to provide fairly for non-farming children while keeping the farm intact. For now, the focus is simple: get the big reliefs right.

Marty Murphy is head of tax at ifac, the professional services firm for farming, food and agribusiness.

SHARING OPTIONS