At first glance, it may look that this deal between Kepak and 2 Sisters is of little direct interest to Irish farmers as it is taking place outside the island of Ireland. However, this deal could be transformative for Kepak and propels them alongside ABP and Dawn Meats in terms of reach and scale.

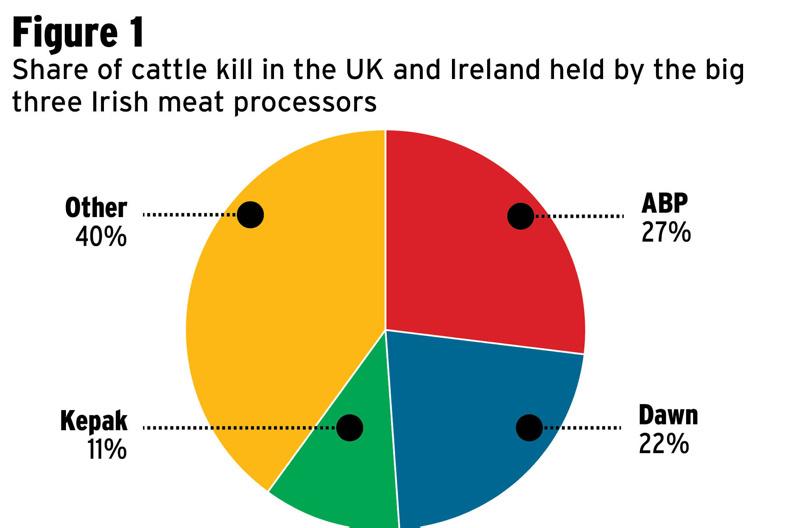

Between them, ABP, Dawn Meats and Kepak now control 60% of the entire combined cattle kill in the UK and Ireland. This would see the three Irish companies processing around 2.7m cattle in total per year.

Recent consolidation

A deal between Kepak and 2 Sisters would be the latest in a recent wave of consolidation that has swept the meat-processing sector in the UK and Ireland. This consolidation has been driven by the Irish meat companies and started when ABP made its move for Bert Allen’s 50% share of Slaney Meats. ABP built on this by acquiring 50% of Northern Ireland processor Linden Foods from Fane Valley.

ABP, along with its interests in Slaney and Linden, now accounts for 30% of the Irish cattle kill, 39% of the cattle kill in Northern Ireland and around 20% of the British cattle kill.

Dawn Meats then acquired Northern Ireland company Dunbia in 2017, giving Dawn a 24% share of the Irish cattle kill, 17% of the cattle kill in Northern Ireland and around 20% share of the British cattle kill.

Up to now, Kepak’s processing interests were exclusively focused in Ireland with operations in beef, sheep and pigs. The group has a 16% share of the Irish cattle kill today. The deal for 2 Sisters red meat division marks a return to processing in the UK for Kepak and will give the group an 11% share of the British cattle kill.

Kepak had previously built a significant presence in Britain at a facility in Preston. Kepak exited processing in the UK in 2007 after exchanging its Preston factory to Dunbia for its processing facility in Kilbeggan, Co Westmeath.

As well as consolidation of meat processors, there has also been an ongoing rationalisation of the supply chains by supermarkets and the major food service buyers.

2 Sisters was subject to an investigation by the Food Standards Agency (FSA) following revelations by a Guardian/ITV investigation late last year on practices in one of their poultry processing factories. The investigation revealed a number of issues around operational process and labelling but recognised that corrective measures had been put in place. Ranjit Singh resigned as chief executive soon after.

Effect of consolidation

When we look at the performance of farmgate prices in Britain compared with Ireland and consider how the foodservice retail and processing chains operate, farmers may be right to question the performance of the meat industry.

The top three supermarkets in the UK (Tesco, Sainsbury’s and Asda) have a combined 58% share of the £185bn UK grocery market and present their beef offering as “British and Irish”.

In their most recent survey in June 2018, AHDB found that Sainsbury had 96% UK beef offering, Asda 55% and Tesco 72%. The same applies with McDonald’s, which has 1,250 stores in the UK and present its beef product offering as British and Irish, while Burger King operates more than 500 stores in the UK.

However, there is currently a 34c/kg differential between the Irish and British beef price (R3 steer), despite the fact that Irish beef retails in the UK at the same price as British beef.

Complexity of beef processing

Factories would point out that they don’t sell every part of the animal to the UK supermarkets or food service sector. The complexity of the business lies in the disassembly of the carcase into a multitude of component parts. The factories then sell each of these in the market where it is valued most, which could be anywhere between the home market for steak meat to the Philippines for lower-value cuts or Africa for byproducts.

SHARING OPTIONS