Over recent years, the Dale Farm business has transformed from a milk brokering co-op selling 60% of its milk pool to today being a fully integrated dairy company processing 85% of its members’ milk. During this period, Dale Farm’s milk pool reduced as producers moved to other processors, this being driven by many factors including not paying a consistent and strong milk price.

With the heavy lifting now done, the farmer-owned co-op has a well-invested processing footprint, a strategy to grow with customers and is actively engaging with farmers to grow its milk pool. Purchasing 800m litres today, not only has it the largest milk pool in Northern Ireland, it is the largest UK farmer-owned dairy co-op in the UK.

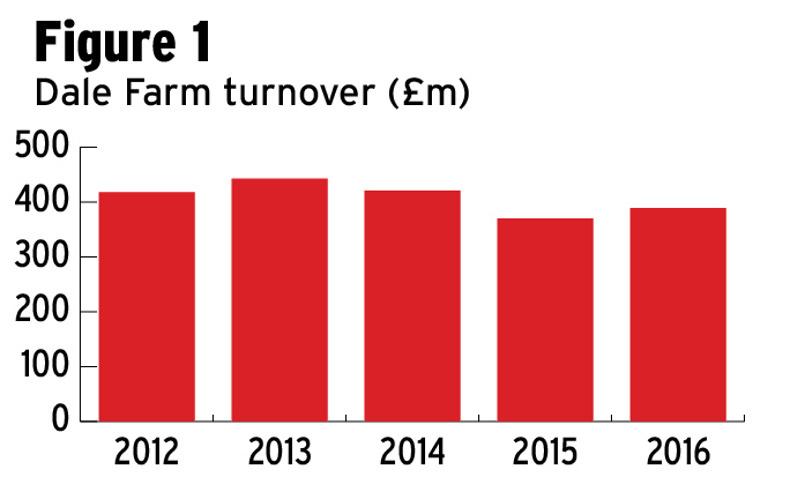

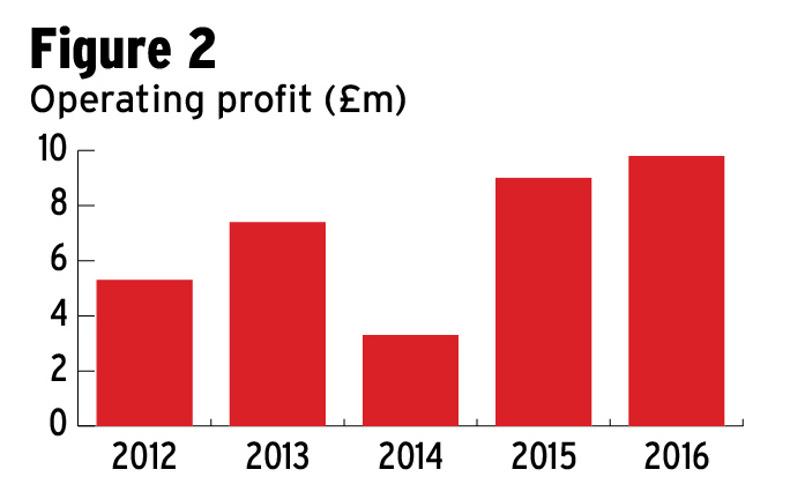

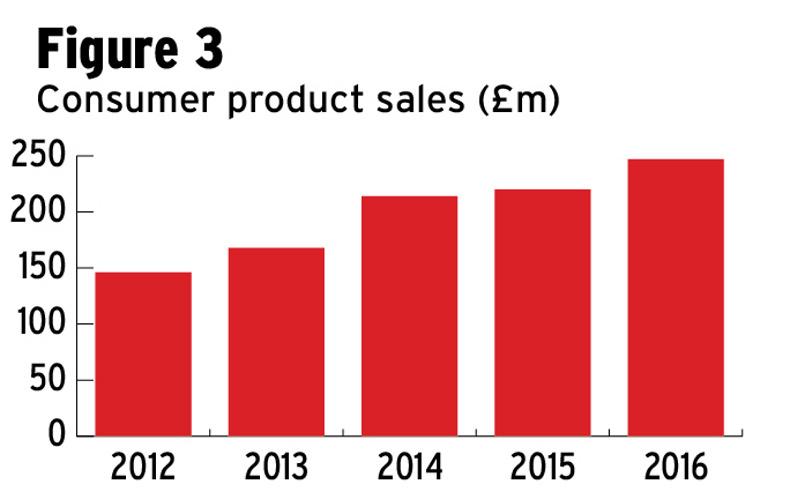

In its most recent set of results announced this week for the year ending March 2017, it reported a solid performance. Operating profit was up 9% to £9.8m, profit before tax increased 16% from £6.8m to £7.9m, with an associated earnings (EBITDA) of £15.9m. Overall group turnover grew by 5.1% to £389m, driven by a 12% increase in consumer sales. The group generated a positive cashflow, with net debt down £2.2m to £64.4m at year end.

Stemming the flow of milk

Undoubtedly one of the biggest challenges facing the business has been to stabilise its milk pool. Over 10 years, the business lost almost 300m, or one-third of its milk pool.

This presented the business, which employs 1,250 people, with the challenge of meeting the growing sales of major UK retail customers. The business has taken action and has actively worked on stabilising the milk pool over the last 12 months by engaging with suppliers, improving productivity at farm level and delivering an improved milk price.

In an unprecedented move for the co-op, the board is now allowing previous suppliers who left to return as milk suppliers. It is also incentivising members to stay through the payment of a 0.3p/litre bonus.

With the milk pool stabilised, it now wants to deliver a consistent and “leading” milk price over time to maintain and grow its milk pool.

This consistency won’t be easy given the markets it plays in. With 55,000t of cheese capacity, Dale Farm is a cheese and whey business at its core, with a butter, liquid milk, yogurt and deserts business along with a feed business.

Consumer foods accounts for over two-thirds (72%) of sales and it processes some 125m litres of liquid milk, with 60% share of the Northern Ireland liquid milk market.

Food ingredients, which includes around 3,000t of whey protein concentrate (WPC), accounts for 14% of turnover. The balance (14%) is in commodities made up of sales of milk powders, bulk cheese and butter.

This is a UK-focused business with half (50%) of turnover coming from Britain, one-third (35%) from Northern Ireland and 15% from outside the UK. This would indicate that the threat of a hard Brexit could present an opportunity to the business given that the UK market is 190,000t short of cheese and 23,000t short of butter.

Acquisitions

Since United Dairy Farmers acquired Dale Farm in 2001, the business has expanded through acquisitions and organic growth. It has since acquired five businesses and has doubled its consumer foods business in the last five years.

In 2002, it acquired Rowan Glen and its milk pool, the market leader in yoghurt in Scotland. Two years later, it bought a desserts business located in Kendal UK from Parmalat. Employing 400 people, it manufactures cheesecakes, trifles, cottage cheese and yoghurts, predominantly for the private-label market.

In 2014, it purchased the Fivemiletown cheese brands from Glanbia, with Glanbia holding on to the milk pool. It leases the factory from Fivemiletown co-op and manufactures soft cheeses such as brie and goat’s cheese. It also acquired Mullins ice-cream business.

One year later, it acquired UK cheese business Ash Manor Cheese. This played a key role in developing its retail strategy. Block cheese from its Cookstown plant is sliced, grated and packed each year at this facility to service the UK retail and foodservice market.

This has led to a scattering of sites across the UK. While it has 10 sites, they are mainly independent operations with no obvious overlaps. Therefore there is limited potential to achieve cost savings through rationalisation. However, if widened to the Northern Ireland processing industry, there may be opportunities to gain some synergies by forming partnerships or collaborations with other co-ops and processors operating in Northern Ireland.

Brands

Dale Farm has brands that go back to the 1950s and subsequently are particularly strong in the Northern Ireland market. For example, Dromona is the number one butter brand, and it also holds the number one ice-cream brand and liquid milk brand in Northern Ireland.

It has the capacity to become market leader across other chilled categories under the brand umbrella across the regions. In Britain, it has focused its growth on own label where it supplies some of the leading supermarket chains. It is estimated that around 65-70% of its business in Britain is own-label.

Debt

Against a backdrop of high debt (£64m), the group is well invested, having spent £60m on new facilities since 2010. The majority of this has been in cheese and whey processing and packing capabilities. The desserts and liquid milk business is also very well invested.

However, net debt is elevated at four times earnings. This is a factor of the business, where the majority of debt in cheese stocks, following the decision a number of years ago to focus on mature cheeses which take 12-18 months ripen.

This creates a high working capital requirement. However, as the stocks are quite liquid, banks are comfortable with this.

One of the down sides of this model, given the recent high level of volatility in dairy markets, is that it creates a high element of risk to the business model. One of the biggest challenges for management is to de-risk the business while capturing the value-add of the mature cheese. For example, the milk it buys today is not sold for 18 months so it is difficult to price.

Management has done a lot to de-risk the model over the last nine months by introducing market adjusters – for example, innovative pricing and developing models that allow it to lay off risk on skim and butter futures markets.

With demand for cheese coming from retailers and especially the discounters, there is significant opportunity for Dale Farm to grow. But to capitalise on this growth it must have a stable and growing milk supply. Farmers no doubt will welcome the decisions it is now taking to address this.

While Dale Farm has collaborations with customers, we could see it opening up the model further. The dairy processing sector in Northern Ireland is categorised by having many small plants and this could involve Dale Farm seeking out collaborations with other co-ops in the future.

While the feed business makes sense in an integrated dairy company and throws off cash, it is more difficult to see how a desserts business sits in the portfolio and adds value to the milk price, before considering health and wellness trends.

With 35% of sales coming from products less than four years old, the business has a proven track record of delivering innovation.

As with any cheese company, the whey for the sports nutrition market is becoming an increasing part of the value add.

A byproduct of this process is whey permeate, which is currently sold to anaerobic digesters. It is welcome to see the business is investigating opportunities to realise this.

Ultimately, farmers will need to see an improved milk price over time to commit increasing volumes of milk to it. In order to help farmers manage volatility, tools such as fixed milk priced schemes will need to be developed.

Well-invested

As it is a consumer business in the main, it should deliver in times of weak dairy markets. While this has not been the case, the fact it is well-invested and has a well-balanced dairy portfolio it is beginning to return to farmers and since August last year it has paid leading milk prices.

Brexit should also act as a tailwind, provided the UK market does not shrink post-Brexit.

SHARING OPTIONS