While beef quotes have improved over the last two weeks, they still have a long way to go to get where both the European and UK trade is at. The Irish prime composite cattle price for week ending November 26 2022 was €4.63/kg deadweight excluding VAT, compared with the EU export benchmark (excluding UK) of €5.00/kg, almost 40c/kg ahead of the Irish composite price. The latest prices reported by Bord Bia for the week ending 26 November is €4.67/kg excluding VAT for Irish R3 steers.

This compares with an average EU price of €5.12/kg and an average UK price of €5.11/kg excluding VAT.

Prices have been moving up in the last two weeks, with short supplies and good Christmas demand leaving factories with no choice but to increase quotes to get cattle.

On a positive note, the average 2022 R3 steer price is currently running at €4.74/kg compared with €4.07/kg for 2021 and €3.63/kg in 2020. However, analysis shows that a beef price of €6/kg is needed for winter finishers to break even over the next few months.

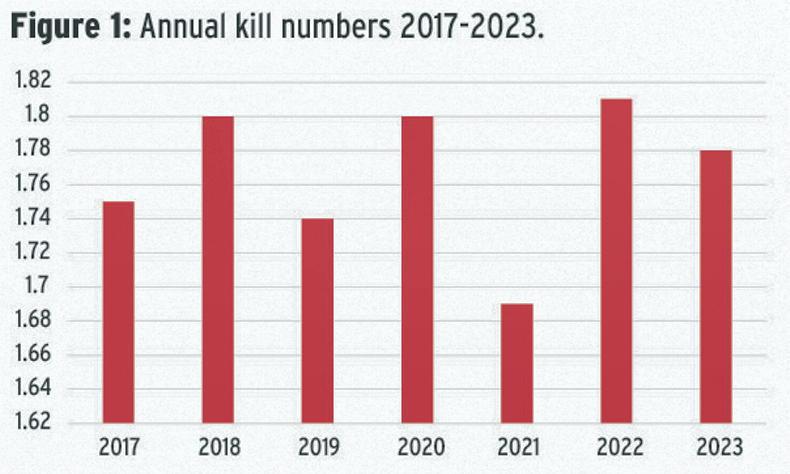

Kill numbers

Taking a look at this year’s kill figures shows that the prime cattle kill is sitting at 1.66m head in 2022. This is up almost 120,000 head or 8% on the same period in 2021.

This excludes the increased number of calves slaughtered in 2022, which was up almost 8,000 head to 28,352 calves slaughtered. The prime cattle kill excluding cows is up 66,000 head to the end of November. The cow kill is up just over 50,000 head on 2021 numbers. Bord Bia estimate that the total kill will end up somewhere around 1.81m cattle. The forecast for 2023 is that the national kill will drop to 1.78m head in 2023, a drop of 30,000 head.

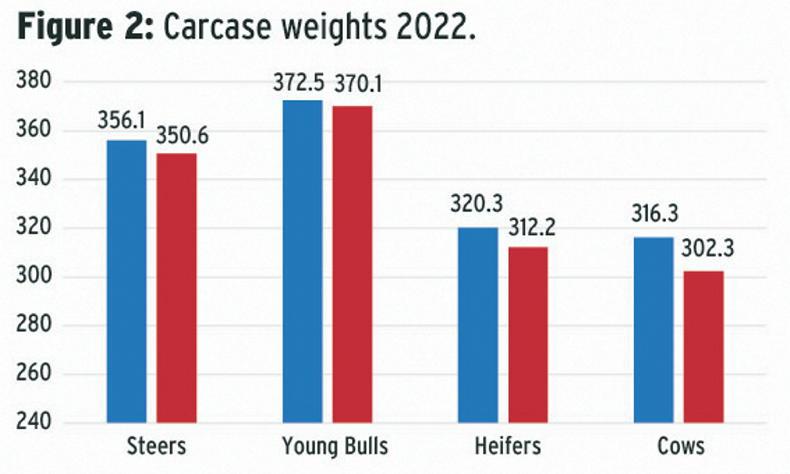

Carcase weights

Figure 2 outlines 2022 carcase weights. We had seen some big movement in weights in 2021, with the downward trend continuing in 2022.

A continuing shift to dairy cross cattle has meant that carcase weights have been reducing for a number of years. Drought conditions in the south of the country and earlier finishing have meant that carcase weights are coming in much lower in 2022.

Cows saw the biggest slip in carcase weights due to a larger proportion of dairy cows being slaughtered in 2022. Heifer carcases were down 8.1kg, while bullocks were back by 5.5kg. Young bulls were back by 2.4kg. This obviously has an effect on beef output, as it takes more cattle to be killed to achieve the same output.

Comment

The outlook for further beef price increases looks positive. Finished cattle are in very tight supply due to a variety of factors. Processors were unwilling to sit down with finishers to talk about prices and contracts at the start of winter 2022. This has caused a lot of smaller finishers to walk away from winter finishing, which means there are a lot less cattle being fed this winter.

During September and October, we saw some very big weekly kills of cattle. This was a combination of cattle being housed earlier and as a result finished earlier. Processors used these higher numbers to their advantage and were able to reduce quotes during that time. This strategy may have come back to bite them, as many finishers looking at beef quotes reducing opted out of purchasing cattle. This has meant numbers coming on stream for the next couple of months will be very tight. Feed costs and high store prices also resulted in some farmers cashing out to avoid incurring huge costs with no guarantee of price in winter finishing.

Beef markets around Europe and in the UK are rock solid, with most countries seeing an improvement in quotes over the last number of weeks. Speaking to the Irish Farmers Journal, Bord Bia’s Joe Burke said: “Beef production is forecast to be down across many European countries in 2023, which should be positive for price.

“Prime cattle supplies are back 3% in the UK so far in 2022, with little change expected in 2023. France, Spain, Italy and the Netherlands are also forecast to be down on production in 2023.

“There is also some pressure on consumption, with retail beef volume sales back by 11%. Food service sales have seen a really strong year, up 26% year-on-year. We are seeing some evidence of consumers buying the same amount of beef in value terms, but with higher prices this has meant lower volumes. We are also seeing some shoppers trading down in terms of purchasing cheaper cuts over the last few months,” he said

In Short

Year-to-date in 2022, Irish R3 steers have averaged €4.74/kg (+17%).So far in 2022, UK R3 steers averaged €5.09/kg (+9%), while across the EU, R3 young bulls averaged €4.93/kg (+25%).Irish prices have fallen significantly since mid-summer and are currently 40c/kg behind our main markets.Irish supplies are strong, including cull cows, although at much lighter weights.Consumer spending power increasingly impacted by inflation.

While beef quotes have improved over the last two weeks, they still have a long way to go to get where both the European and UK trade is at. The Irish prime composite cattle price for week ending November 26 2022 was €4.63/kg deadweight excluding VAT, compared with the EU export benchmark (excluding UK) of €5.00/kg, almost 40c/kg ahead of the Irish composite price. The latest prices reported by Bord Bia for the week ending 26 November is €4.67/kg excluding VAT for Irish R3 steers.

This compares with an average EU price of €5.12/kg and an average UK price of €5.11/kg excluding VAT.

Prices have been moving up in the last two weeks, with short supplies and good Christmas demand leaving factories with no choice but to increase quotes to get cattle.

On a positive note, the average 2022 R3 steer price is currently running at €4.74/kg compared with €4.07/kg for 2021 and €3.63/kg in 2020. However, analysis shows that a beef price of €6/kg is needed for winter finishers to break even over the next few months.

Kill numbers

Taking a look at this year’s kill figures shows that the prime cattle kill is sitting at 1.66m head in 2022. This is up almost 120,000 head or 8% on the same period in 2021.

This excludes the increased number of calves slaughtered in 2022, which was up almost 8,000 head to 28,352 calves slaughtered. The prime cattle kill excluding cows is up 66,000 head to the end of November. The cow kill is up just over 50,000 head on 2021 numbers. Bord Bia estimate that the total kill will end up somewhere around 1.81m cattle. The forecast for 2023 is that the national kill will drop to 1.78m head in 2023, a drop of 30,000 head.

Carcase weights

Figure 2 outlines 2022 carcase weights. We had seen some big movement in weights in 2021, with the downward trend continuing in 2022.

A continuing shift to dairy cross cattle has meant that carcase weights have been reducing for a number of years. Drought conditions in the south of the country and earlier finishing have meant that carcase weights are coming in much lower in 2022.

Cows saw the biggest slip in carcase weights due to a larger proportion of dairy cows being slaughtered in 2022. Heifer carcases were down 8.1kg, while bullocks were back by 5.5kg. Young bulls were back by 2.4kg. This obviously has an effect on beef output, as it takes more cattle to be killed to achieve the same output.

Comment

The outlook for further beef price increases looks positive. Finished cattle are in very tight supply due to a variety of factors. Processors were unwilling to sit down with finishers to talk about prices and contracts at the start of winter 2022. This has caused a lot of smaller finishers to walk away from winter finishing, which means there are a lot less cattle being fed this winter.

During September and October, we saw some very big weekly kills of cattle. This was a combination of cattle being housed earlier and as a result finished earlier. Processors used these higher numbers to their advantage and were able to reduce quotes during that time. This strategy may have come back to bite them, as many finishers looking at beef quotes reducing opted out of purchasing cattle. This has meant numbers coming on stream for the next couple of months will be very tight. Feed costs and high store prices also resulted in some farmers cashing out to avoid incurring huge costs with no guarantee of price in winter finishing.

Beef markets around Europe and in the UK are rock solid, with most countries seeing an improvement in quotes over the last number of weeks. Speaking to the Irish Farmers Journal, Bord Bia’s Joe Burke said: “Beef production is forecast to be down across many European countries in 2023, which should be positive for price.

“Prime cattle supplies are back 3% in the UK so far in 2022, with little change expected in 2023. France, Spain, Italy and the Netherlands are also forecast to be down on production in 2023.

“There is also some pressure on consumption, with retail beef volume sales back by 11%. Food service sales have seen a really strong year, up 26% year-on-year. We are seeing some evidence of consumers buying the same amount of beef in value terms, but with higher prices this has meant lower volumes. We are also seeing some shoppers trading down in terms of purchasing cheaper cuts over the last few months,” he said

In Short

Year-to-date in 2022, Irish R3 steers have averaged €4.74/kg (+17%).So far in 2022, UK R3 steers averaged €5.09/kg (+9%), while across the EU, R3 young bulls averaged €4.93/kg (+25%).Irish prices have fallen significantly since mid-summer and are currently 40c/kg behind our main markets.Irish supplies are strong, including cull cows, although at much lighter weights.Consumer spending power increasingly impacted by inflation.

SHARING OPTIONS