The west Cork co-ops are once again setting the pace when it comes to the July milk price. All four (Drinagh, Barryroe, Bandon and Lisavaird) lifted milk price 0.13c/kg milk solids (MS) or the equivalent of 1c/l for July supplies. In effect, it means for July the west Cork milk prices are on average 0.33c/kg MS (or 2.6c/l) ahead of the bigger national players. July is a big milk supply month for spring milk producing dairy farmers.

The other big move in July was that the traditional lower division players (Lakeland, LacPatrick, and Kerry) all lifted milk price by 0.13c/kg MS (1c/l). Aurivo lifted milk price 0.06 c/kg MS (0.5 c/l), while the rest held June price. Hence for July, LacPatrick, Lakeland and Kerry jump above the major players in the east and south, Glanbia and Dairygold. Glanbia lifted milk price 2c/l for June supplies so they will argue the rest are only catching up.

All processors who lifted milk price acknowledged that the positive July moves are reflective of steady milk markets, with slowing global milk supply growth and reasonable demand. US milk supply for July 2018 was 17.3bn pounds, up 0.4% from July 2017. New Zealand milk supply only really gets going in August.

This week, severe rain is causing flooding and difficult grazing for many parts of New Zealand, especially in the North Island. The big European milk countries are likely to have reduced feed supply, which could also impact on milk supply over coming months.

Average July price

The average price for the main table is €4.37/kg MS, which is equivalent to about 31c/l at 3.3% protein and 3.6% fat ex-VAT. Weighted for volumes per processor (because only 5% of national milk is in west Cork) the average is probably closer to €4.28, so in effect the base price ex-VAT at 3.3% protein and 3.6% fat is closer to 30c/l ex-VAT.

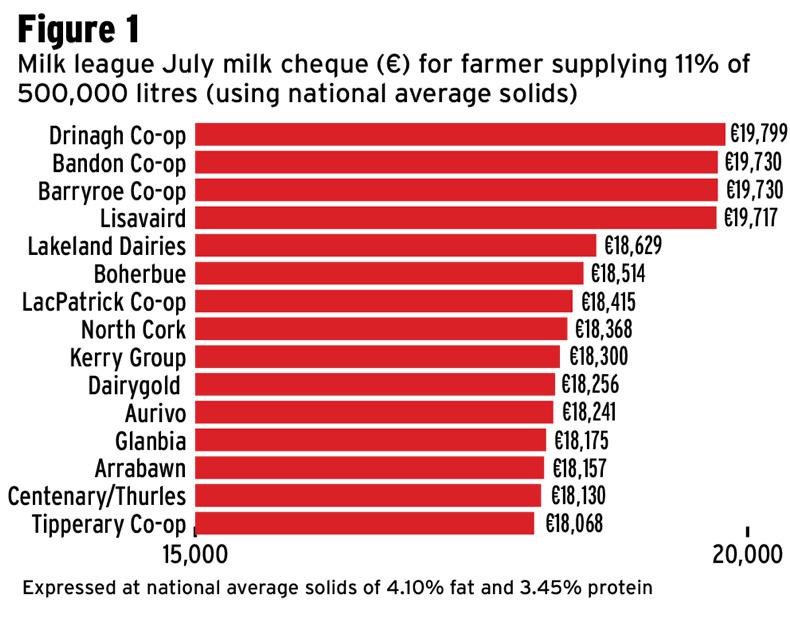

It also means for the July milk cheque there is now a difference of over €1,500 between the top and bottom of the league when we compare them all at the same milk solids (Figure 1). Put that on top of the €6,800 cumulative differences from April to June and it means a farmer supplying a processor in the lower divisions compared to the top is down over €8,300 or €80 per cow for the average Irish herd over the last four months.

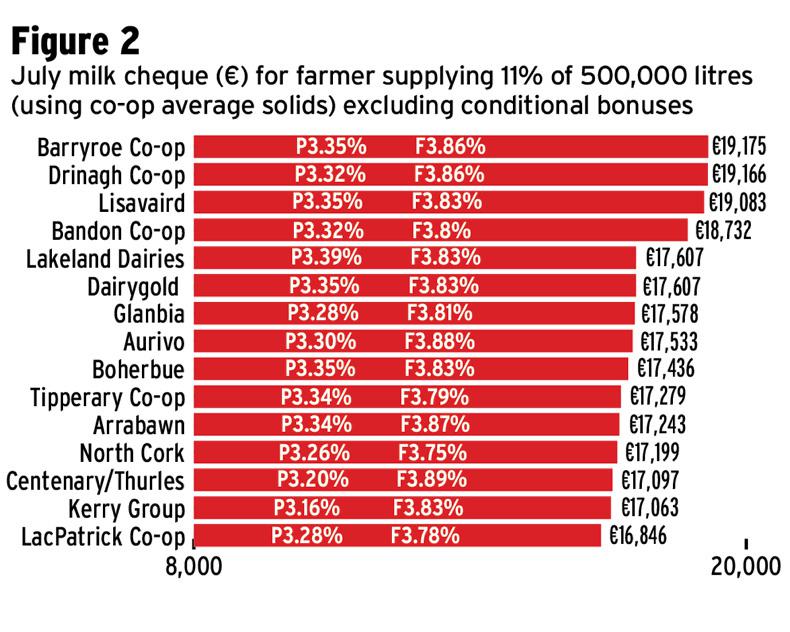

Figure 2 shows the differences for the July milk cheque accounting for the differences in fat and protein between processors.

SHARING OPTIONS