Record low supply headlines the summary of a subdued farmland market in the UK for 2019. Continued political and economic uncertainty again weighed on the market as Brexit deadlines and elections made for better viewing than participation.

Farmland values remain steady and our analysis of those active in the market suggest new motivators are influencing demand for farm and amenity real estate.

2019 farmland values

Market uncertainty

Farmland values remained largely flat during 2019, as the market continued to grapple with uncertainty.

The Savills Farmland Value Survey shows that average values have been relatively static, with the average for all types of farmland across Britain falling 0.2% to £6,687/acre.

The average value of English farmland dropped 0.4% on 2018 figures, whereas Scotland and Wales recorded gains of 0.5% and 1.2%, respectively.

Northern England recorded the largest value increase of 1.3% in contrast to a 1.2% loss across the east of England.

Across Britain, while average prime arable land recorded a 0.5% drop to £8,715/acre, prime dairy farmland values gained 0.8% to £6,767/acre. These fairly static values may partly be due to reduced market activity. However, Savills sales show evidence of a wide range of prices achieved either side of the average, which suggests a continuation of dynamic market forces.

2019 farmland supply

Farmland market supply reached a record low in 2019, with just 117,000 acres publicly marketed across Britain. This eclipses the previous record of 135,000 set in 2012 and is the lowest since Savills starting tracking the farmland market in 1993.

Last year’s farmland supply was down 38% on 2018 (189,000 acres) and down 29% on the five-year average.

Reduced offerings were a common theme across Britain, with Scotland recording a 44% drop in supply to 25,000 acres, Wales a 32% reduction to 8,231 acres and England a 37% decline to 85,000 acres.

The largest fall in publicly marketed sales occurred in the east of England, where only 11,000 acres were marketed, – 67% down on 2018 and about half the long-term average.

Buyers and sellers

Analysis of transactions during 2019 where Savills acted for either the buyer or seller shows that in a smaller market, new non-farmer buyers represented a higher proportion of buyers in 2019.

These represented 23% of all purchasers compared with 16% in 2018, which is the highest proportion for five years. This suggests that current purchasing motivators are more aligned to lifestyle and investment security than commercial farming.

Indeed, 55% of new farm buyers cited residential or sporting interests as the key motivation for the purchase, with investment motivating another 21%.

Taking existing non-farming buyers into account, non-farmers accounted for 53% of all purchasers.

Evidence from our agents around the country shows that non-farming investors continue to show interest in acreage close to regional centres or with the potential for diversified business opportunities.

Commercial farmers with successors showed continued appetite to expand across quality farmland or in locations well-suited to complement existing farms.

Full-time farmers represented just 36% of all sellers – the lowest level since our records began in 1993

Farmers represented just 42% of all buyers, which is the lowest level since our records began.

Our research of sellers shows a clear link between farming activity and the amount of land being publicly marketed.

Full-time farmers represented just 36% of all sellers – again, the lowest level since our records began in 1993.

Clearly, regulatory uncertainty has overwhelmed the decisions to sell for some time. However, those who did sell may have grasped an opportunity as demand for the right properties has remained strong. Almost half of farmer-sellers cited either retirement (17%) or investment outside of farming (30%) as a reason to sell.

Non-farming landowners represented around half of all sellers, with motivations similar to selling a private residence – relocation, downsizing, death/personal reasons and financial restructuring.

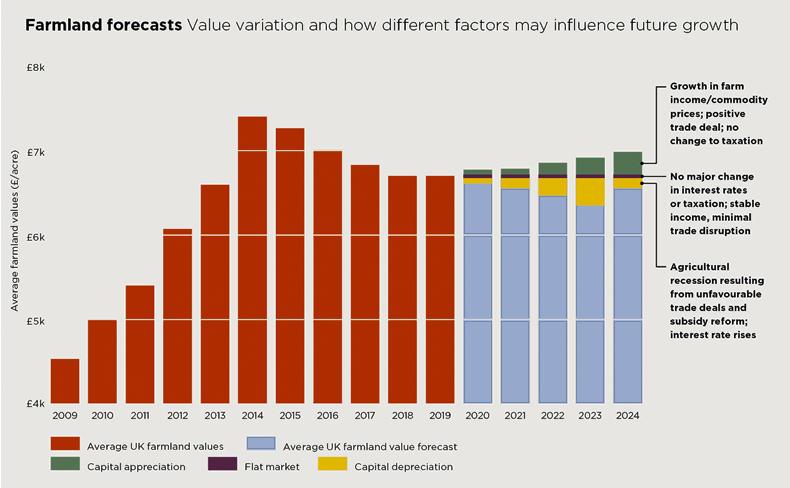

Farmland forecast

The 2020 farmland forecast is delivered with greater confidence following the decisive election result on 12 December 2019.

Although the general election is a small part of the bigger story that is still playing out, a strong Conservative majority implies continuity in the farm business environment, even if a great deal of regulatory change faces the sector over the coming five years.

The forecast identifies the major influences that, in combination, could create three possible market scenarios over the next five years – an appreciating market, a static market and a depreciating market.

The outcome of trade deals is the major macroeconomic factor to be determined, and more clarity over domestic policy is expected in the coming months.

Overall, we predict that the broader economy is more likely to perform positively in the next five years, at least once the first Brexit hurdle is passed.

With the UK population set to rise by 5% over the next decade, demand on food, energy and water systems is unlikely to abate

Therefore, we expect the capital appreciation scenario will prevail for land, with local factors remaining the predominant influence on land values.

In any event, we predict the upside potential of capital appreciation to be greater than any potential reduction in average values in a capital depreciation scenario, largely due to environmentally oriented demand for land underpinning the lower end of the market.

With the UK population set to rise by 5% over the next decade, demand on food, energy and water systems is unlikely to abate.

Land is a finite resource in the UK and with numerous competing land uses under pressure to grow, we consider any major contraction in land values unlikely.

NB: Our forecasts are subject to political and economic forces that are somewhat uncertain at the time of writing. Should any significant change in these factors occur, these forecasts may be revised to consider the result.

SHARING OPTIONS