The Irish Farmers Journal publishes weekly tables of prices paid in Irish factories for steers, heifers, young bulls and cows across a range of grades. This week, we combine the returns for 2016 and will rank all Irish beef processing factories in order from the highest to lowest prices per kilo.

Factories that kill more than 20,000 cattle annually are obliged by law to report prices to the Department of Agriculture Fisheries and the Marine (DAFM). These are in turn forwarded to Brussels, as is the case with every other member of the EU. This enables accurate comparisons be made between prices paid across the EU on a weekly basis. The data compiled by DAFM from the individual factory returns is made available to the Irish Farmers Journal and published this week.

When we published the aggregated league tables in July 2015 and 2016, they reflected the position mid-year. This is now being moved to a calendar year.

The leagues are based on the midpoint of each grade, namely U=3=, R=3=, O=3= and P+3= across steers, heifers, young bulls and cows, with VAT included at 5%.

What is behind the price paid?

Looking at factory beef prices purely on the place in the league table could be seriously misleading. Final prices paid by factories for cattle reflect everything that is judged by them to be of value in the market. Therefore, farmers need to make sure they match the type of stock they have with a factory that is actually anxious to buy their type of cattle.

For example, if a factory is top of its league table for a particular grade of steers, it is important to find out what exactly they want before dropping cattle into the lairage. If a factory has strict weight limits and insists on Quality Assurance (QA), a farmer supplying non-QA heavy cattle runs the risk of penalties. In such an example, it may well be that one of the factories lower down the league table overall might in fact be paying a better price for what are described as out-of-spec cattle. This is because it is are likely to be selling to lower-value markets, outside the UK supermarkets, which pay less money but are in turn less fussy.

Feedlot and contract cattle

Factories that own or contract-feed large numbers of cattle can influence the overall average that they pay. In these arrangements animals are bought and finished to tight specifications and usually at a premium price. When there are large numbers of these going into a particular factory, this has the potential to affect the overall average paid, making it look higher than it actually is if farmer suppliers are paid less.

Impact of niche cattle

The biggest niches in the Irish beef industry are the speciality breeds which are paid a premium by some factories. Aberdeen Angus is the most common of these, with Herefords in second place. Shorthorns also came on the scene in 2016. A dedicated supply group was established, but it is in its early stages, with low numbers compared with the other two. Organic production also remains low, but at times has the potential to distort overall reported averages.

In examining the actual prices paid in factories, the factors that determine price become clear. We can also immediately see trends emerging, with companies that have very specific purchasing requirements topping tables in one category but close to the bottom in other categories where they aren’t actively buying.

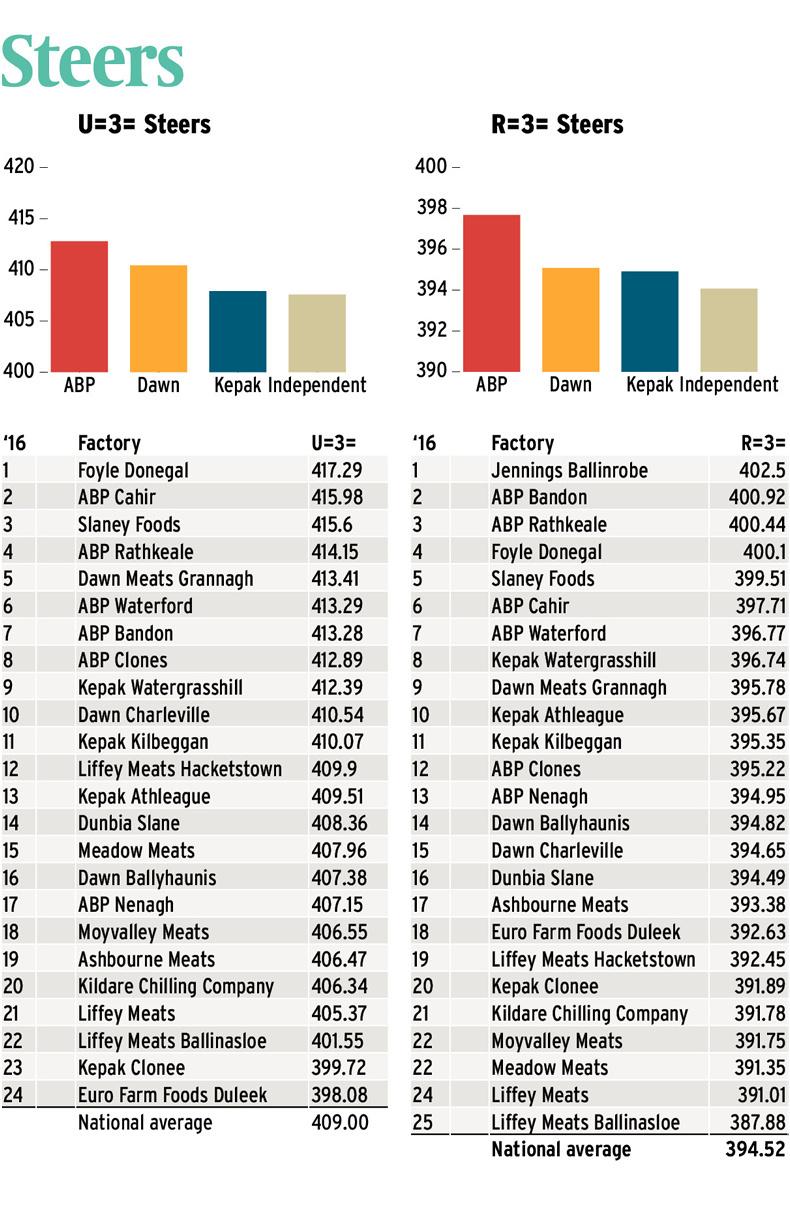

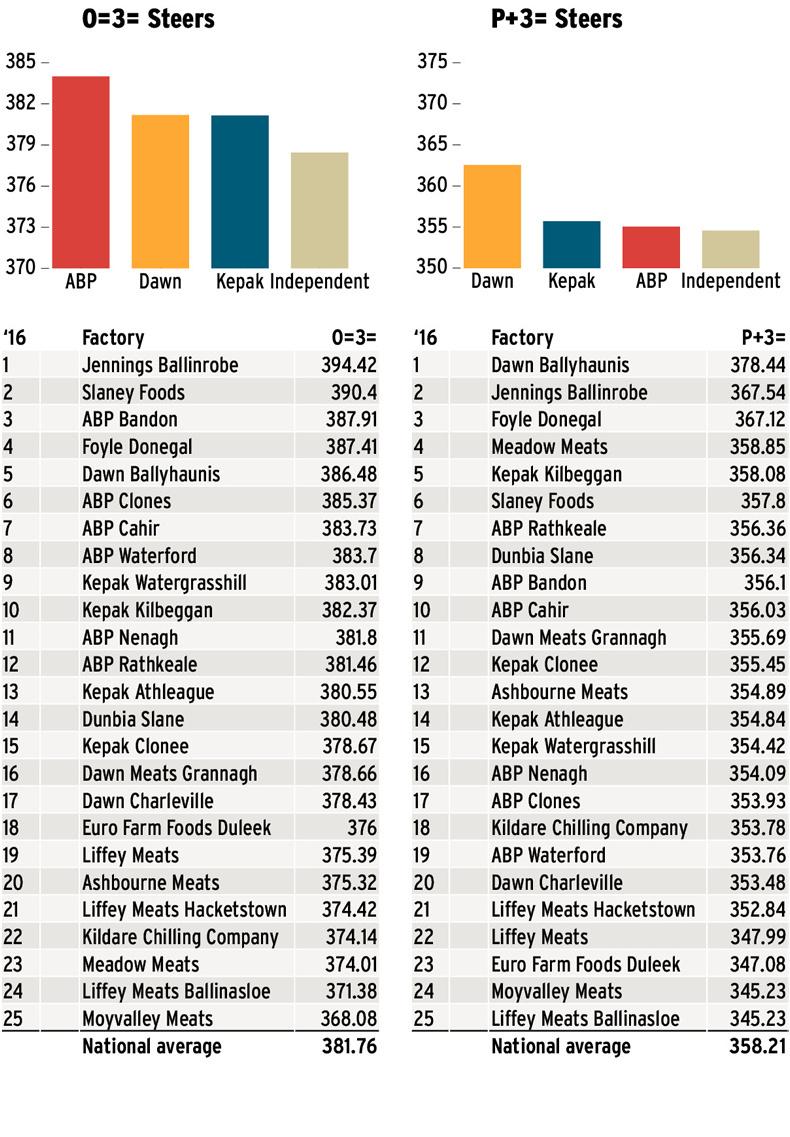

Steer beef is considered the flagship product of the Irish beef industry, with the price ranges in the tables being 19c/kg on U=3= grades, 15c/kg on R=3=, 26c/kg on O=3= and 33c/kg on P+3= grades. The gap is particularly large in the P=3= category but if we look at the gap between first and second place, we see a 9c/kg differential. This probably reflects the fact that the P category of steers is small overall and the top price paid is probably on a small number of cattle.

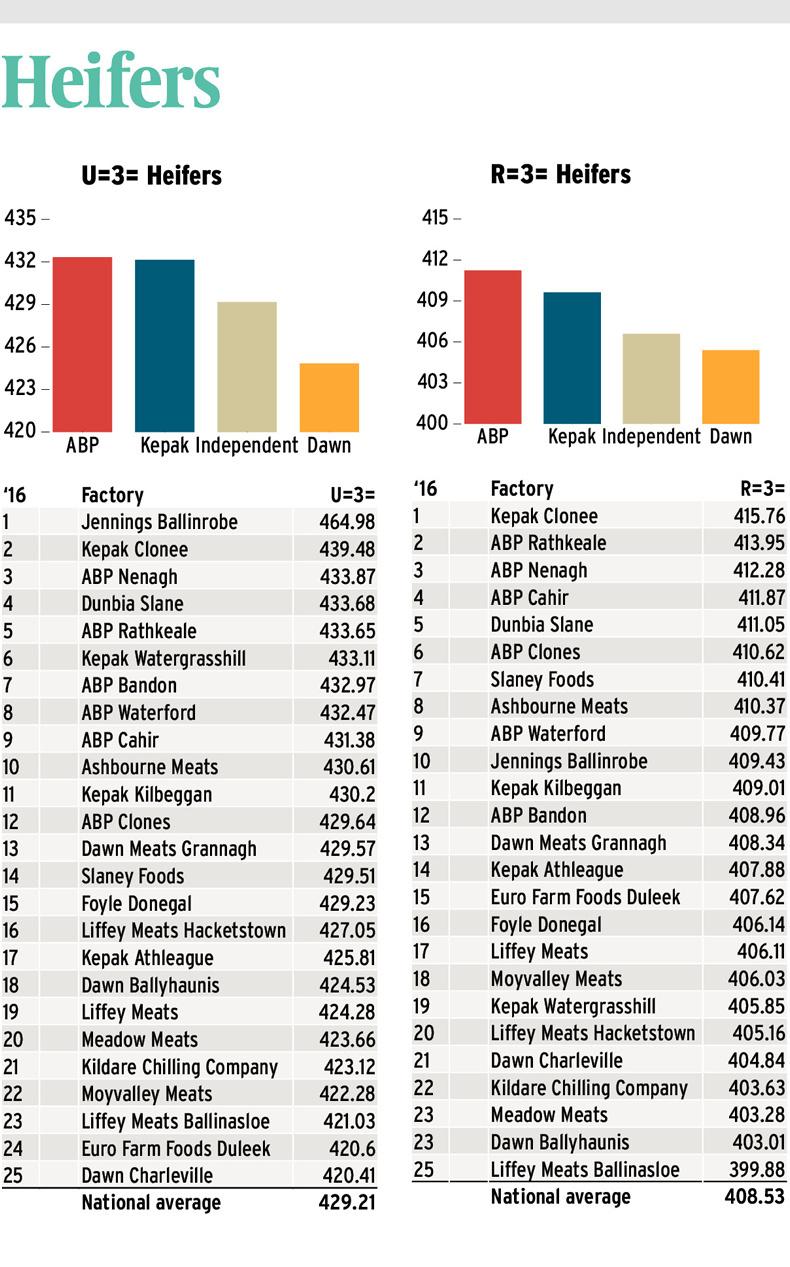

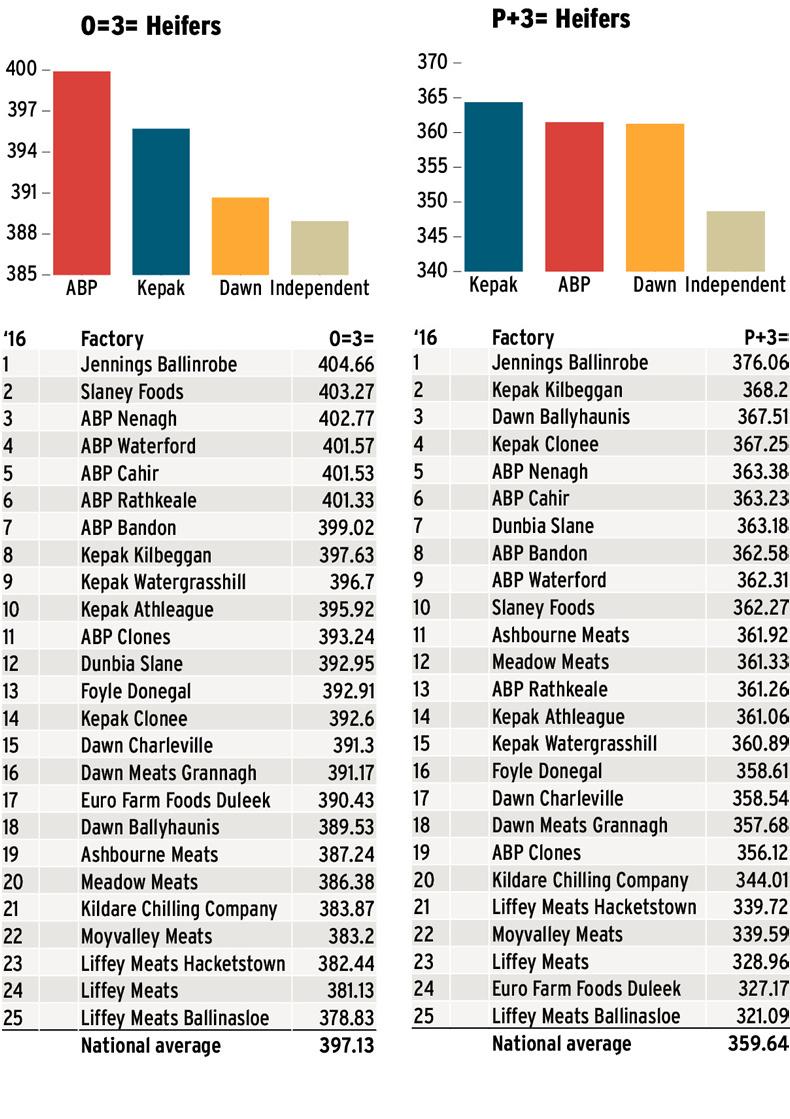

There is a huge price spread on U=3= heifers of over 44c/kg but again attention has to be drawn to the wide gap between top and second place in the table of 25c/kg. The majority of grades fall into the R and O categories, so numbers are likely to influence this gap. On R=3= heifers, the spread between top and bottom is just over 15c/kg while on the O=3=, the gap is 26c/kg. Again, the relatively small number of P+3= heifers will have influenced the spread, which is 55c/kg.

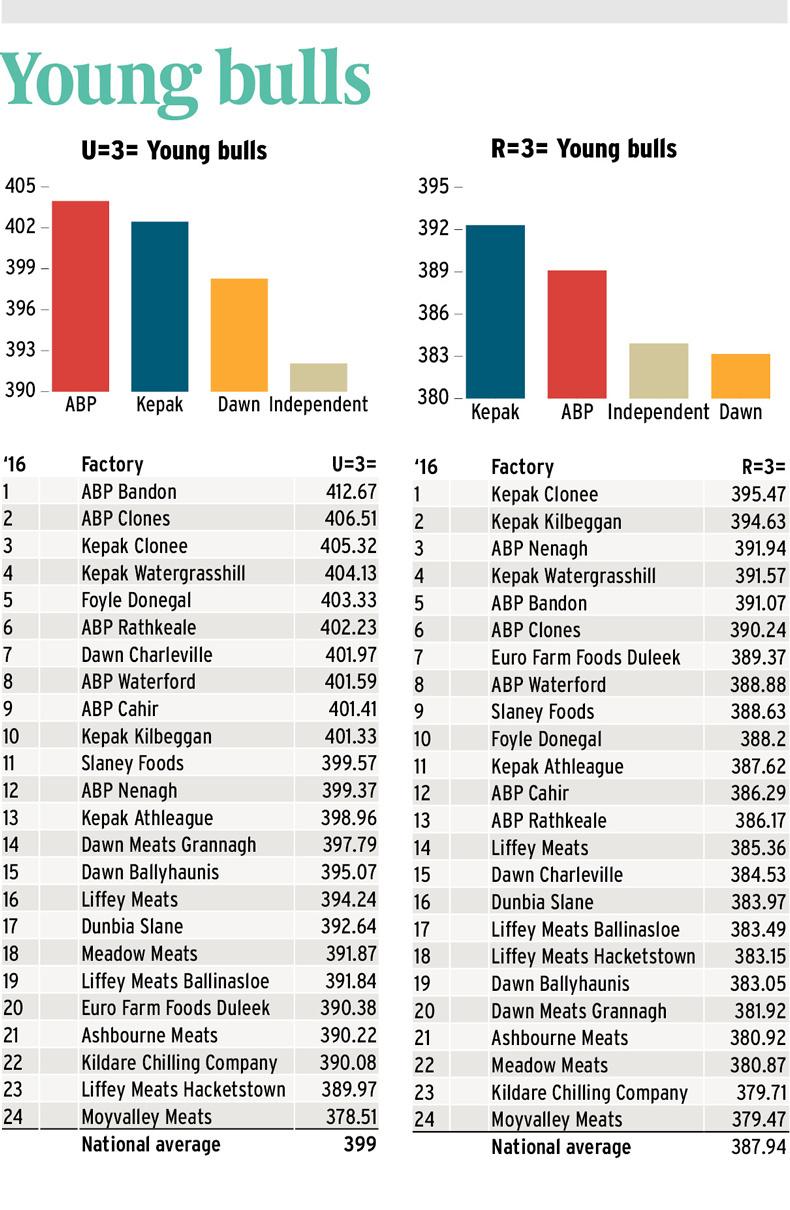

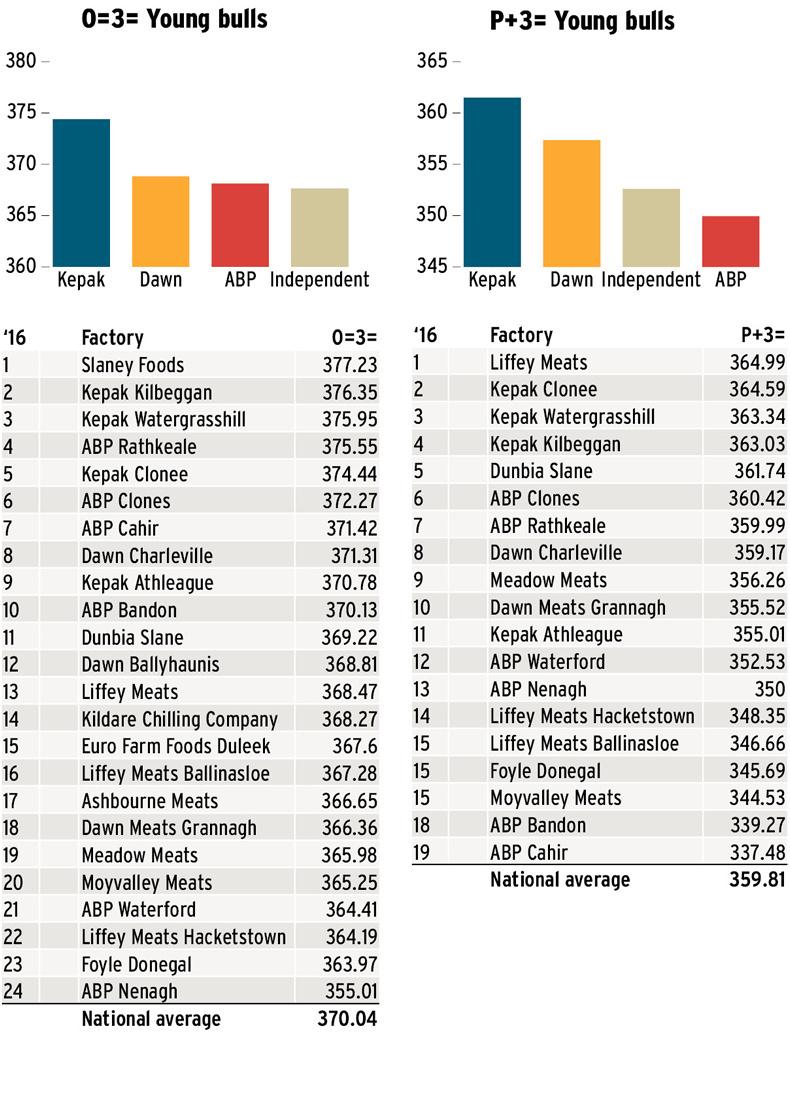

The significant thing about young bulls that isn’t reflected in the tables is the fact that there are two categories of young bull. Bulls under 16 months are usually bought on the grid while bulls between 16 and 24 months tend to be bought flat on a price for Us and Rs. With that in mind, there is a spread of 34c/kg between top and bottom places on U=3= young bulls, while the R=3= young bulls have a spread of just 16c/kg. On the P+3= young bulls the spread is 27c/kg but the notable point in this category is the fact that six factories didn’t have any in this category to report at all over the entire year. O=3= spread is 22c/kg.

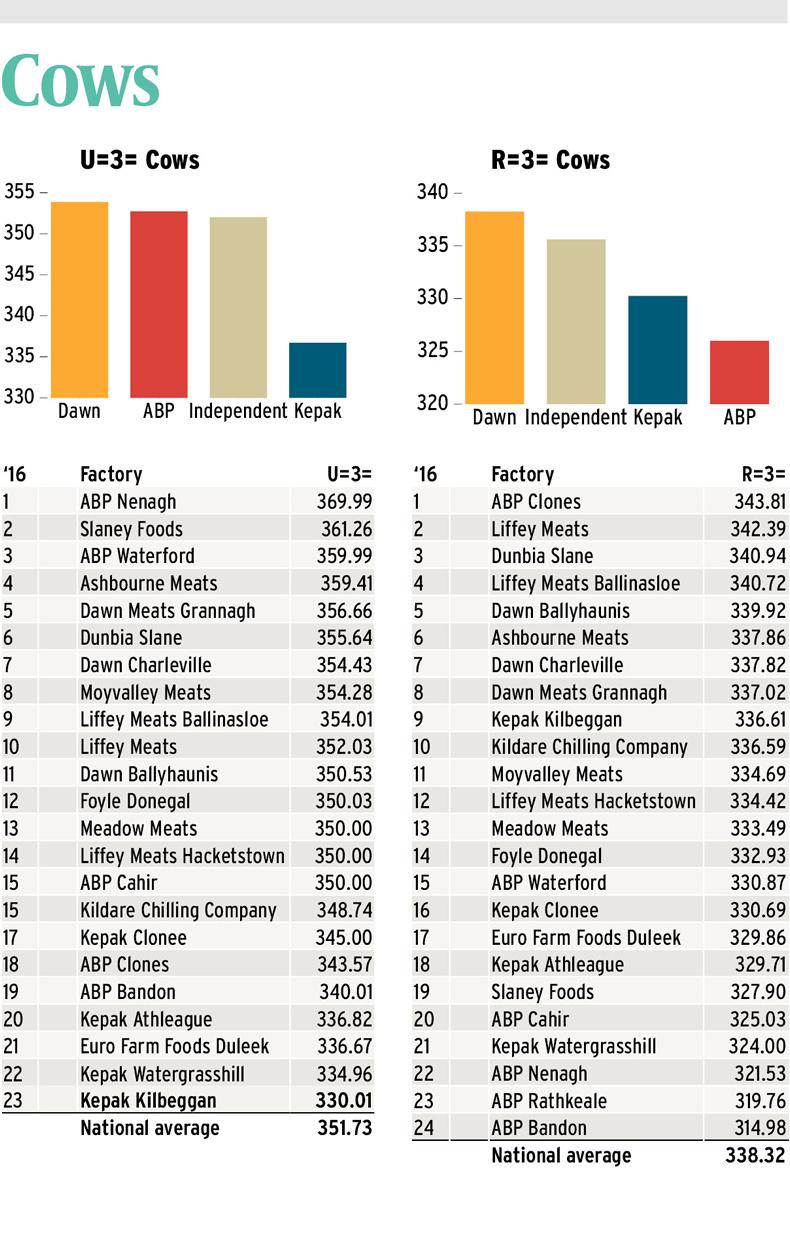

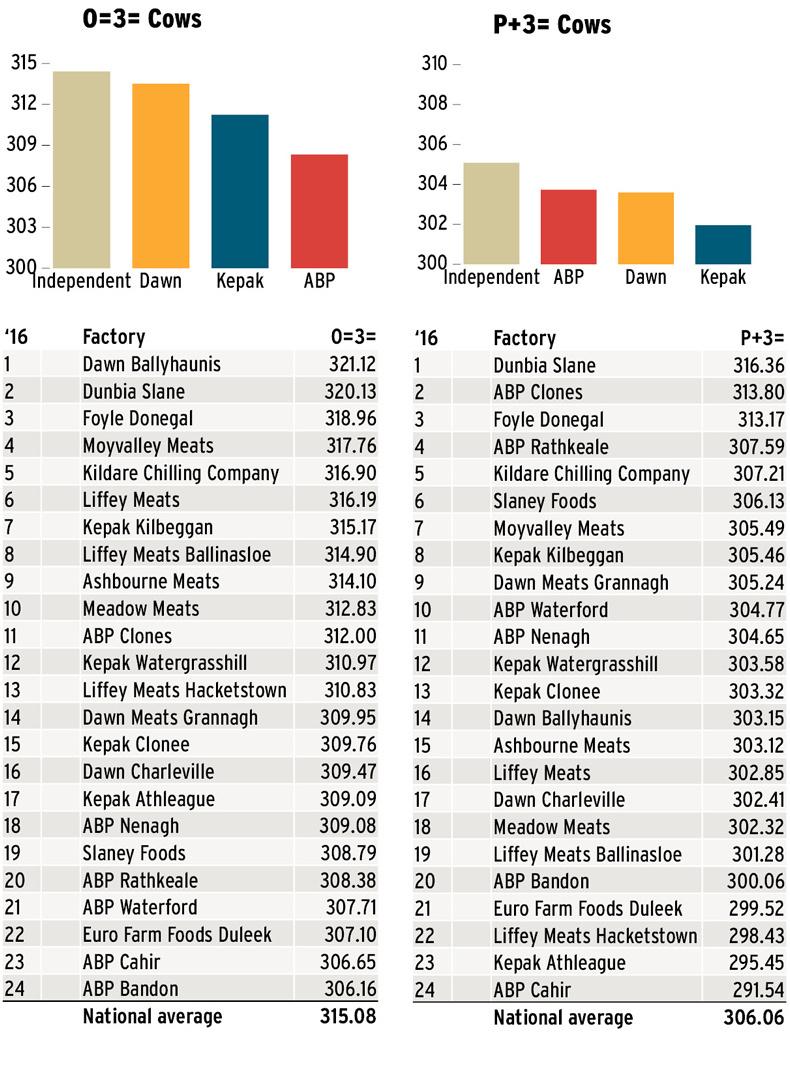

Processing cows is one area where Irish factories excel, with farmgate prices consistently at the top end in Europe along with France. Cows tend to be bought on weight in Irish factories to three basic categories – butcher cows are the well-finished heavier cows, steaker cows are plainer but have some cover and the blue or canning cows are typically straight out of the parlour into the factory. They are, however, price-reported like all other categories and show a price spread of 40c/kg on the top U=3= cows (with two factories not killing any of these), 29c/kg on R=3= cows, 15c/kg on O=3= cows and 25c/kg on P+3= cows.

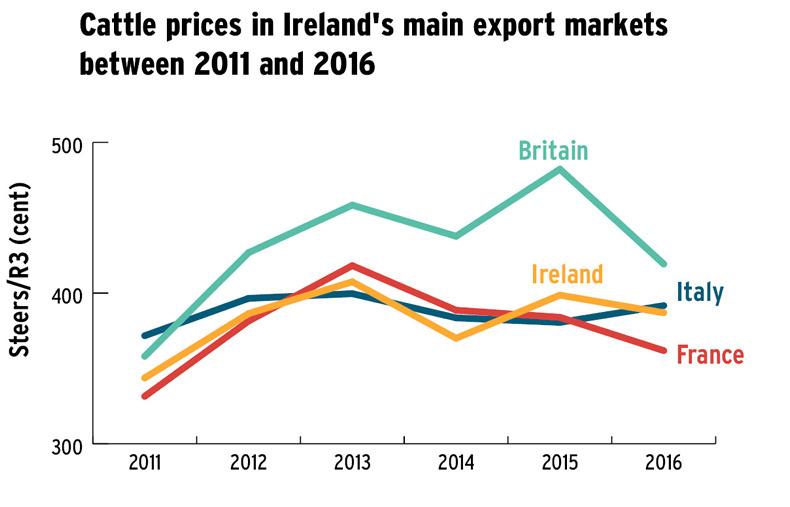

Irish beef volumes increased in 2016 by 5%, reflecting the growth in cattle numbers, driven by dairy herd expansion ahead of milk quotas being abolished in 2015.

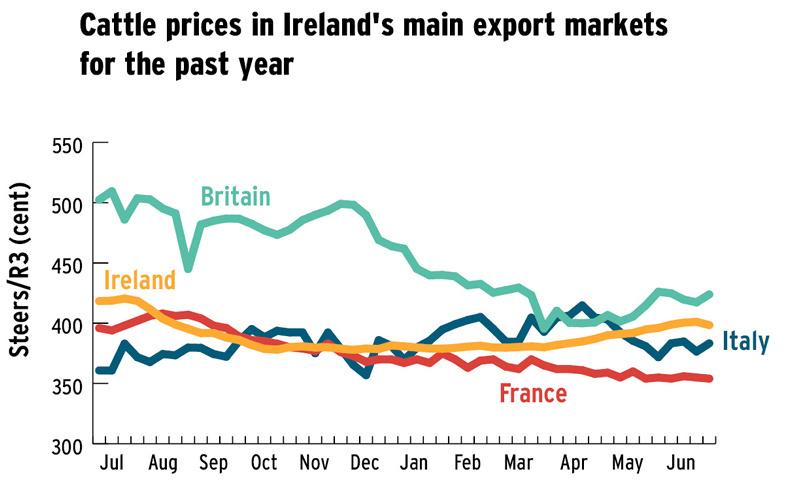

The main market remains the UK, taking 270,000t in 2016 followed by France on 62,000t, the Netherlands on 50,000t and then Italy on 31,000t. Irish prices opened the year 80c/kg behind British prices on R3 steers but 5c/kg ahead of France, 53c/kg ahead of the Netherlands and equal to Italian prices. The gap with Britain closed in the first half of the year until it was almost eliminated. This was driven by the weakening of sterling in the runup to the Brexit vote in June. Thereafter, despite sterling weakening further, the gap widened again as British prices increased and Irish prices fell. By the end of the year, the gap between Irish R3 steers and British R3 steers was 55c/kg.

Elsewhere, as the Irish weekly kill remained around 35,000 cattle, Irish prices also fell behind prices paid to farmers for cattle in our other main export destinations with the exception of the Netherlands. French R3 young bulls were worth 4c/kg more than Irish while Italian R3 young bulls were 37c/kg ahead of Irish R3 steers at the end of 2016.

The Netherlands, which grew as an export destination by 10,000t in 2016, had a farmgate beef price consistently behind Ireland, starting the year 49c/kg behind on R3 young bulls compared with Irish R3 steers and that gap remained throughout the year.

SHARING OPTIONS