Beef

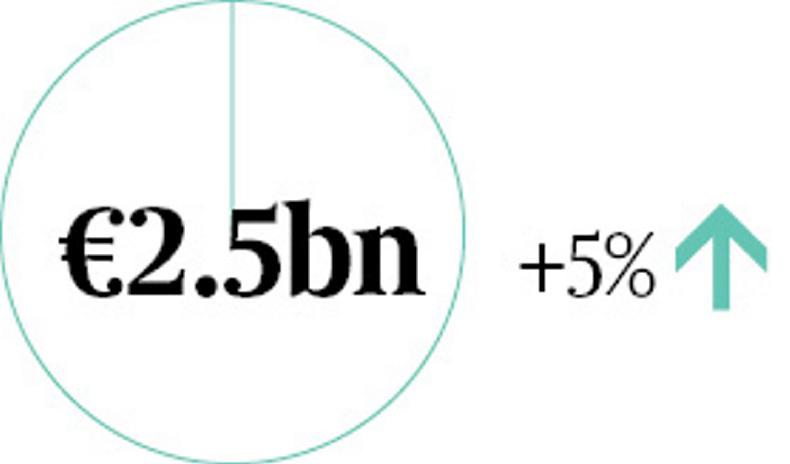

In 2017, Irish beef exports were valued at €2.5bn, an increase of 5%.

As projected, the volume of Irish beef production increased by 4.5% in 2017 to 615,000t.

Supplies of cattle rose by 100,000 head in 2017. However, the impact of higher cattle supplies was partly offset by a decline in carcase weights. Up to the end of September, carcases were running 3.5kg lighter on average versus the same period in 2016.

Total exports for 2017 rose to an estimated 556,000t and the UK remains the number one destination, accounting for 51% of beef exports. Other EU countries accounted for 43% of exports and beef exports to international markets rose to 6%.

Dairy

Irish dairy exports increased by 19% in 2017 to €4.02bn, an increase of €655m. Butter was the main driver of dairy export growth in 2017, with values up 62% to €879m.

Increased milk production and higher dairy market returns were the drivers of export growth last year, with strong growth to leading markets including the Netherlands, Germany, France and Belgium.

Exports to non-EU markets increased by 9% to almost €1.8bn, with trade to the North American market growing by 7% to €270m. China, at €65m, accounts for 37% of non-EU dairy trade and 16% of total dairy exports.

Despite a fall in the value of sterling, the value of dairy shipments to the UK grew by 15% to €968m.

Specialised nutritional powders remain the leading dairy export at about €1.3bn. The largest increase is for butter, which rose by more than 60% to nearly €900m, driven by high demand and prices on EU and international markets.

Sheep

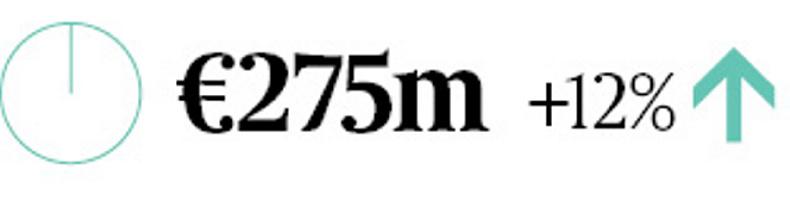

In 2017, the value of sheepmeat exports grew by 12% to €275m.

Irish sheep numbers passed the 2.94m head mark in 2017 – a 10-year high – while sheepmeat exports for 2017 are expected to reach 57,000t, a 14% increase year-on-year.

Over 42% of exports were destined for markets other than France and the UK in 2017.

Thanks to a weaker sterling, UK exports have had a particularly strong year, with indications that export volumes will be up by 15,000t on the previous year.

At €4.80/kg, average producer prices were marginally back by 5c/kg on 2016, largely due to an overhang of hoggets.

Securing market access to non-EU markets of US and China remains a priority and will help manage the carcase balance of cuts to offal.

Live animals

Bord Bia estimates that live exports increased by 21% in 2017 to €175m – with €115m of this accounted for by live cattle.

Overall cattle exports for the year reached approximately 190,000 head in 2017, up from 145,000 head the previous year.

Calf exports dominated the trade in live cattle shipments, and the decline of 2016 was reversed during 2017 with a 40% growth rate to over 101,000 head.

The Turkish market opened to Irish cattle in autumn 2016 and in 2017 almost 30,000 animals were exported there. Turkey now accounts for 16% of the Irish live cattle trade.

Live cattle exports to Britain were 11% below 2016 levels, at just 6,000 head. However, more than 27,000 cattle were sent to Northern Ireland – a 12% increase.

Overall live pig exports rose 16% year-on-year to €53m, with the main market being Northern Ireland.

Live sheep exports were very similar to the previous year and remained at about €8m and 48,000 head. Religious festivals continue to play an important part in the sheep trade.

Poultry

The overall value of Irish poultry exports increased by around 3% for 2017 to €295m. However, volumes only increased by 1% during the same period. The number of birds processed in Ireland reached record levels at 96m.

The vast majority of Irish poultry exports continue to go to the UK, which recorded almost 80% market share for 2017 or some €240m.

The share of Irish poultry exports going to other EU markets has edged upwards to 10%, with France maintaining its position as the most important market, especially for leg meat that is not consumed on the home market.

The key challenges facing the Irish poultry industry are Brexit and bird flu, according to Bord Bia.

Increasing market access is a key priority for the sector.

However, some recent developments to open trade could lead to new opportunities, such as the EU-Japan free trade agreement.

Pigmeat

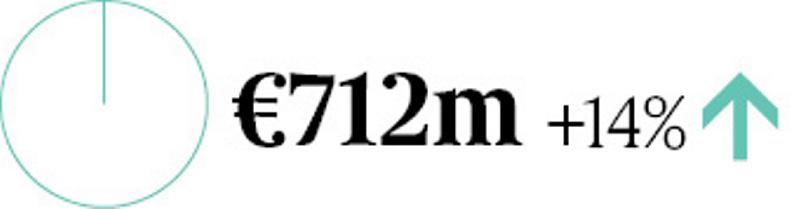

Pigmeat exports rose 14% in value in 2017 to over €712m, driven by higher prices in EU markets.

Export meat plant pig supplies in Ireland are estimated to remain steady at around 3.3m head during 2017. Bord Bia identified Brexit as a key challenge for the pig sector. The UK remains by some distance our main trading partner in this sector and new and expanding markets outside of the UK will be required to protect against Brexit.

The pigmeat industry also faces challenges due to animal health related issues. These relate to both processed meat products and the use of antibiotic drugs in herds and consequent antimicrobial resistance.

Horticulture and cereals

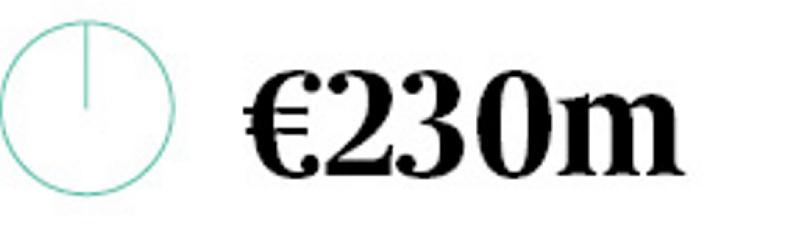

The overall value of the edible horticulture and cereals export market for 2017 remained largely flat year on year at some €230m, according to Bord Bia.

At €91m, the mushroom sector remains the single biggest export and has also recorded flat growth for 2017. The cereals sector, predominantly barley and oats, declined sharply – by some 9% to €69m – although it still remains the second most important product within the category.

Other vegetables have grown steadily to €13m, up 7%, while potato exports reached in excess of €5m.

Butter drives 2017 food exports to new highs

Analysis: China and Asian markets vital for Irish meat industry

SHARING OPTIONS