Finished cattle have become scarce in the past two weeks, leading to an increase in beef prices.

Official kill figures from DAERA show that the prime cattle kill in NI this year is running slightly ahead of 2016, with 79,553 steers, heifers and young bulls slaughtered over the last 12 weeks, compared with 76,400 in the same period in 2016.

However, much of the difference in slaughter numbers came in the early part of the year, with some strong kills during January. The evidence suggests that finishers decided to market cattle earlier, perhaps partly in response to market trends in 2016 and 2015 when beef prices came under pressure in the spring.

As a result, cattle are coming out at younger ages, with recent analysis from the Livestock and Meat Commission (LMC) highlighting that the average age at slaughter for steers to date in 2017 is 23.9 months, compared with 24.6 months in the same period in 2016.

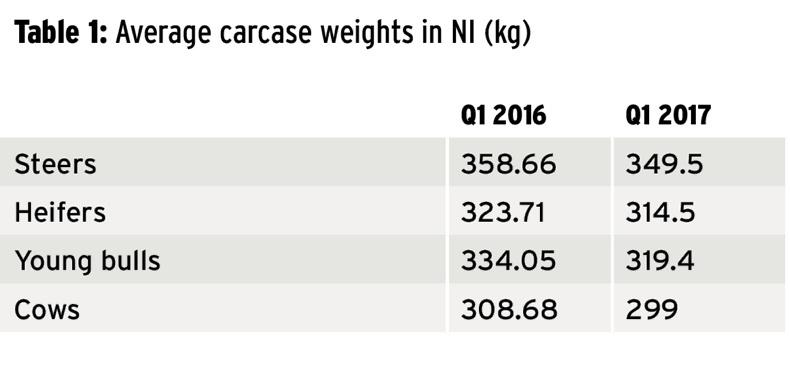

With cattle marketed earlier, and in response to penalties on overweight cattle, carcase weights at slaughter are also down (Table 1) which effectively means there is less beef going into store.

Taking everything together, and with beef sales staying relatively strong, the market in NI has moved in favour of producers at present.

However, at the start of 2017, reports suggested that finished cattle numbers would be strong throughout the year.

In January, LMC cattle forecasts for the first quarter (Q1) of 2017 estimated that just over 86,000 prime cattle would be presented for slaughter (the actual figure was 85,430), up around 6,000 on Q1 in 2016.

Forecasts for Q2 and Q3 of 2017 are also higher when compared with 2016.

An extra 5,000 head is expected to come on to the market in Q2 compared with 2016, taking the total prime kill to 81,055.

Forecasts for Q3 are about 2,000 ahead at 72,182.The kill is expected to rise to 90,716 for Q4, only slightly ahead of the 90,336 in 2016.

The majority of the additional cattle expected in Q2 and Q3 will come from increased numbers of beef-sired, dairy-bred animals.

There are currently around 2,500 more beef-sired dairy calves aged 18 to 24 months on farms compared with this time last year and an extra 5,000 beef cattle aged 24 to 30 months still to be processed.

Market outlook

The beef market here will continue to be heavily influenced by the market in Britain.

Forecasts for beef markets there indicate domestic production will contract by 2% to 890,000t this year mainly as a result of lighter carcase weights and a drop of 8% in the cow kill.

The euro-sterling exchange rate will also be a factor for the year ahead.

Weaker sterling makes NI beef more price-competitive on the continent, and Irish beef less competitive in the UK market.

SHARING OPTIONS