My husband came home from the Ploughing last week and said he was buying a tractor. He didn’t go there to buy one. When I asked him did we really need it, he said it was a great way of saving tax for this year and there was a good no-interest finance deal. I work off-farm and support the house and our children, one of whom is in college. I’m getting tired of it. Money is always tight and I spend my time budgeting and trying to make ends meet. We have not been on a good holiday in years, as the farm always seems to need more and more investment. Would it not be better to pay the tax rather than to commit ourselves to more borrowing?

Jane

There was certainly plenty of things to tempt farmers at the Ploughing last week and not everything was what farmers need.

When I rang Jane to discuss the situation, she said her husband Brian was a dairy farmer and they had built the herd up to about 80 cows. They had not been to their accountant this year to confirm what the actual tax bill would be. She said she never goes and Brain just tells her what the situation is when he comes back.

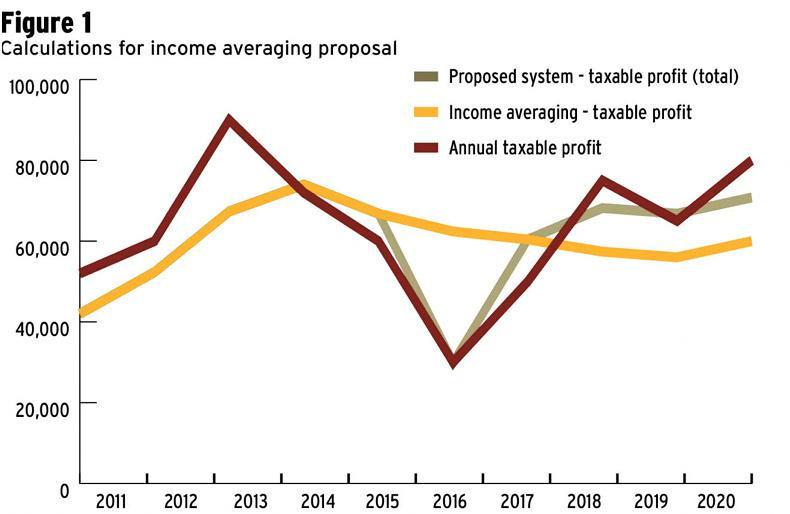

The first thing I said was that she should go to the meeting, as it would help her understand the farm business and the decisions like investments and tax planning. Most dairy farmers are facing a larger tax bill this year due to a rise in profits over the last three years. It means the final tax payment for 2013 will be higher that what was paid in preliminary tax last year. This will also have a knock-on impact on the preliminary tax to be paid by the end of October. Income averaging will help, but many farmers are facing a much larger tax bill. That doesn’t mean a knee-jerk reaction to purchasing a tractor or anything else should be done. You should arrange a meeting with you accountant as soon as possible. The aim is to establish your exact balance of tax for 2013 and likely tax for 2014.

The first question you should ask is are other tax allowances being used to minimise the tax bill? As you are married with dual income, you can earn up to €65,600 (see table) at the low rate of tax. However, if you are earning lower than €23,800, you will receive the standard cut-off rate of €41,800, plus the amount of income you earn. As Jane earns €20,000, it would mean the top rate of tax is paid at €61,800. The farm could attribute income of €3,800 that would be taxed at lower rate. They have one child over 16 and he works on the farm. They can pay him up to €8,250 a year tax-free, but remember USC and PRSI would have to be paid.

The biggest question to ask is, does buying the new tractor makes economic sense? Does the farm really need it and what extra profit will it generate? The second important question is, can the farm actually afford it?

There is no such thing as zero finance, as the cost is paid by someone. Part of it is normally included in a higher purchase price, compared with what you would pay if you had hard cash.

The real danger for your husband, and many like him, is the risk to the business if income is much lower next year due to weather or lower milk price. Income averaging will work against him and put pressure on cashflow.

I am not one to talk down milk prices, but you have to be realistic. With milk quotas going there is bound to be a lot more volatility in milk prices and income for dairy farmers. To look at how exposed your business is, you have to look at overall costs and repayments.

Ask your accountant to look at the profitability of the farm if the milk price went as low as 28c/litre. Would you have enough money to make loan repayments? Should the aim be to set aside money to cover a situation like this? As your children grow up and go to college the money needed will increase. It does seem that the farm needs to contribute more to the household bills. This has to be considered alongside any planned expenditure and expansion.

If your farm has high profitability and high tax bills, in the long term it may be worth looking at a limited company structure. Many farmers in Brian’s situation will find that if they are planning expansion it might not make sense. The reason is capital allowances will reduce the tax bill for a number of years. We are moving into a new era in dairy and with it comes the need to learn new skills. Managing the risk will be vital and putting much more thought into buying the new tractor should be the start of it. CL

KEY POINTS

• Don’t make a knee-jerk reaction to avoid tax.

• Visit your accountant and know what questions to ask.

• Make sure all tax allowances are availed of.

• Risk has to be managed in the future.

• Look at the impact of volatility.

• A cash fund is a good idea to protect against volatility.

SHARING OPTIONS